I’ve seen so many people get confused or anxious whenever they hear the phrase “tax brackets.” I was definitely one of them.

When I first filed my own taxes, I had this overwhelming sense of responsibility, and I was sure all my salary would get wiped out by taxes.

So today, let’s talk about the 2025 tax brackets. We’re going to break down these complex things into simple, easy-to-understand terms.

What Even Are Tax Brackets?

Think of the 2025 tax brackets like a cake. You don’t eat the whole cake in one bite (unless you’re having a really bad day, of course!). You cut it into slices, and each slice is taxed at a different rate.

The first slice (your lowest income) is taxed at the lowest rate. As you move up, new chunks of your income get taxed at a higher rate.

It doesn’t work like this: The IRS sees your $80,000 salary and says, “Oh, you’re in the 22% bracket? Great, we’ll tax all $80,000 at 22%.” That’s a myth. Only the part of your income that falls into the 22% bracket gets taxed at 22%. The rest is taxed at the lower rates. This is called a progressive tax system. (IRS.gov)

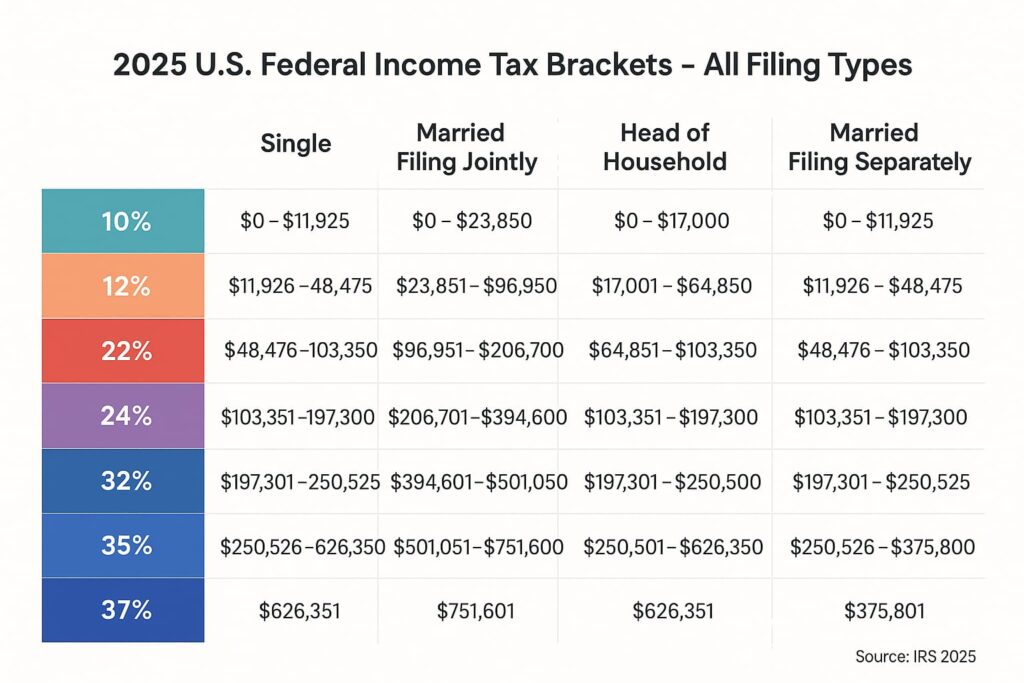

Federal Tax Brackets 2025: The Numbers You Actually Care About

Let’s get into the real numbers. These are the IRS’s 2025 federal income tax brackets, with some real examples! These calculations are all accurate.

The numbers are a bit different if you’re married filing jointly, head of household, etc., but the basic concept is the same.

If you’re interested in the details for Married Filing Jointly, Head of Household, or Married Filing Separately, let me know and I can provide a detailed breakdown for those categories.

Let’s Do the Math (Without the Headache)

Let me give you a personal example. When my income was $50,000, I was worried that a big chunk of it would be taxed at the 22% rate. I had some reasons for thinking that, but it turned out to be completely wrong.

Here’s how it actually worked:

- The first $11,600 was taxed at 10% = $1,160

- The next $35,550 was taxed at 12% = $4,266

- The final $2,850 (the part above $47,150) was taxed at 22% = $627

- Total tax = $6,053

So yes, I was in the “22% bracket,” but most of my money was still taxed at the lower 10% and 12% rates. That’s a huge difference, and I hope it makes sense now.

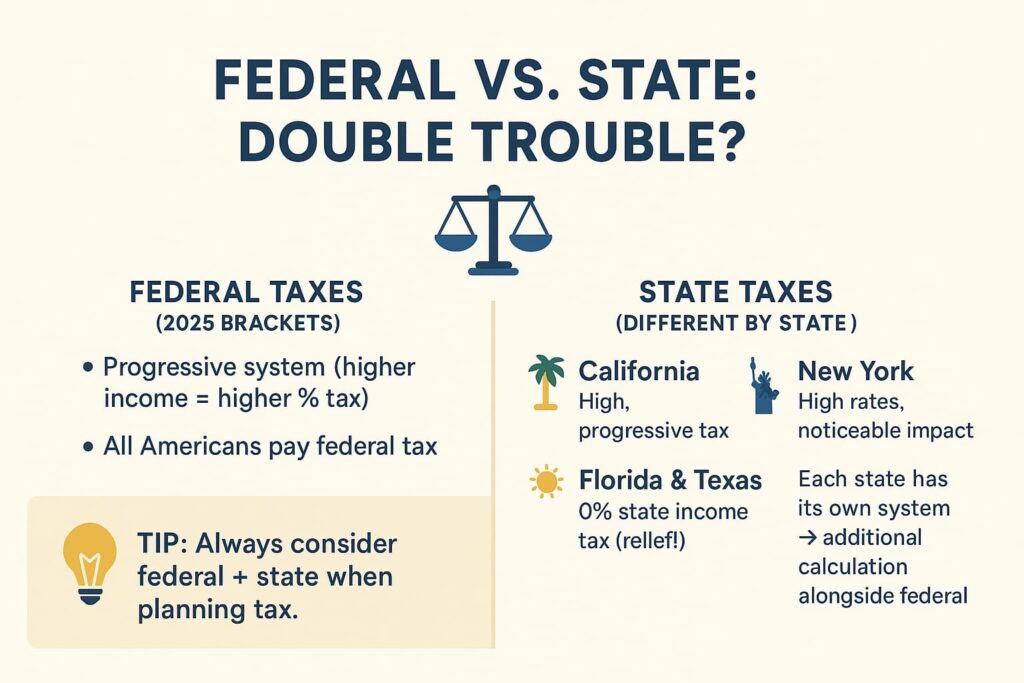

Federal vs. State: Double Trouble?

Here’s where it gets a little tricky. The 2025 federal tax brackets are only half the story. Your state also wants a piece of the pie.

- Live in California? You’ll have to pay state tax, and that’s also a progressive system.

- Live in Florida or Texas? Congratulations, there’s no state income tax there!

- New York? Let’s just say you’ll definitely feel it.

My advice is to never stop at just the federal taxes when you’re planning. Always check your state’s tax system, too.

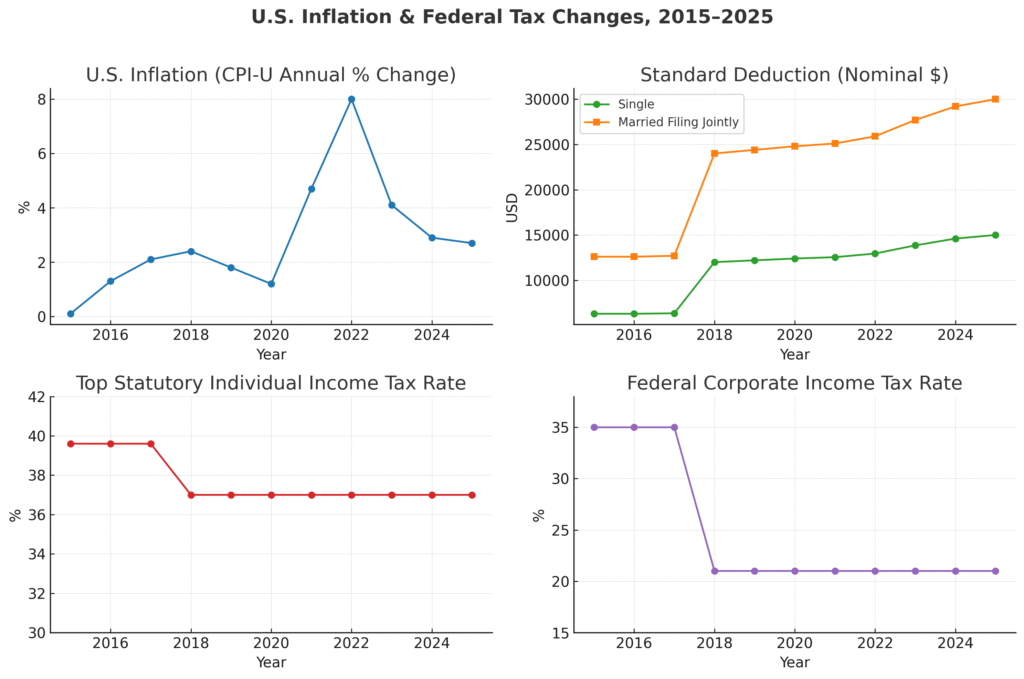

What Changed in 2025?

One good thing the IRS does is adjust the brackets for inflation every year. Without these adjustments, we would all end up in the 37% bracket without even earning much more money.

Here’s the breakdown of the past 10 years in this chart.

There have been some minor changes for the 2025 tax brackets, but the good news is that most people’s income will continue to fall into the lower brackets.

How to Play It Smart

You can use tax brackets to your advantage. Here are a few things that worked for me:

- Max out your 401(k) or IRA. This lowers your taxable income. When I started contributing an extra $2,000 to my 401(k), a portion of my income actually dropped into the 12% bracket.

- Understand the standard deduction. For 2025, it’s $14,600 for single filers and $29,200 for married filers. The IRS lets you off the hook for this amount entirely.

- Look into credits. While deductions lower your taxable income, credits directly reduce your tax bill. The Child Tax Credit, Earned Income Tax Credit, and education credits can all make a big difference.

If you want to learn about deductions, tax credits, child tax credits, and all of these topics, then this guide will be very useful for you. In this guide, we’ve tried to explain everything in very simple language.

The Health Savings Account (HSA)

If you qualify, you get three major benefits:

- Tax-free contributions

- Tax-free growth

- Tax-free withdrawals (for qualified medical expenses)

Learn more about HSAs (HealthCare.gov)

Additional Benefits:

- Portability (it stays with you even if you change jobs)

- Rollover (unused funds carry over each year)

- Retirement advantage

- Investment options

2025 Contribution Limits (according to the IRS):

- Individual coverage: $4,300

- Family coverage: $8,550

- Catch-up (age 55+): An extra $1,000

Simply put, an HSA is a “tax-free health and retirement piggy bank.” If you qualify and can afford to contribute, it’s considered one of the best tax-advantaged accounts in the U.S.

Qualified Medical Expenses (For HSA)

- 🏥 Doctor & Hospital

- 💊 Medicines & Treatment

- 👓 Dental & Vision

- 👶 Pregnancy & Family

- 🩺 Other Health Services

- 🏠 Medical Equipment

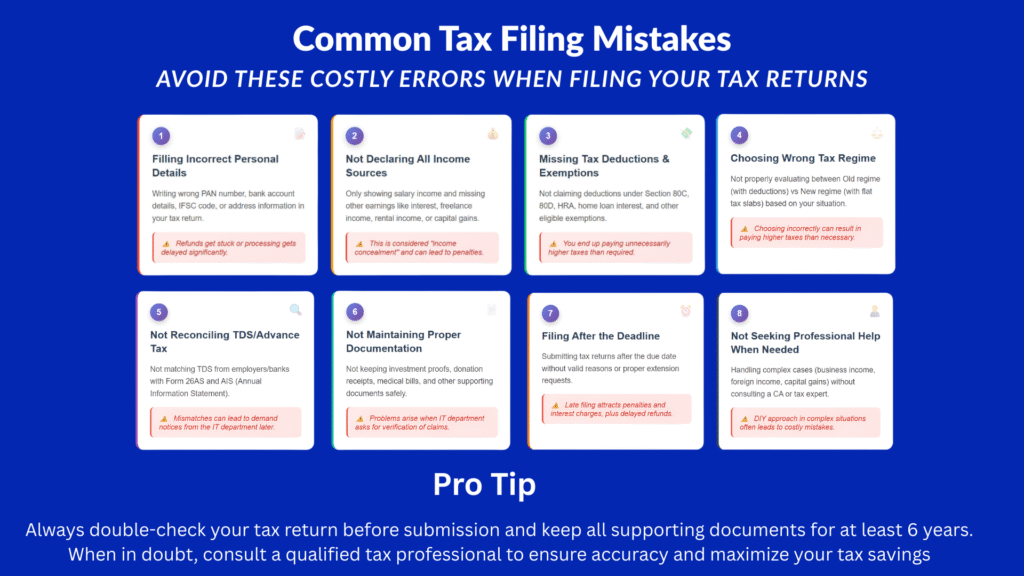

Common Mistakes When Filing Taxes

- Filling out the wrong personal details

- Not declaring all your income

- Missing out on exemptions and deductions

- Choosing the wrong tax regime (Old vs. New)

- Not reconciling TDS/Advance Tax payments

- Not saving your proof of documents

- Filing late

- Not getting professional help when you need it

Myths That Drive Me Crazy

- “If I move into a higher tax bracket, I’ll lose money.” (Wrong) You still keep more of your money. Only the extra income is taxed at the higher rate.

- “Federal and state taxes are the same.” (Nope) They are completely separate systems. Some states don’t even have an income tax!

Wrapping It Up

If I can share my own experience, the 2025 tax brackets aren’t as scary as people make them out to be. Once you understand the “cake slice” analogy, you’ll be able to handle your taxes with a lot more confidence.

April used to be a month of panic for me. Now? I quickly run my numbers, see where I stand, and make small moves, like increasing my retirement contributions, to keep more money in my pocket.

If you’re still confused, that’s okay. Use an online tax calculator (Nerdwallet) or talk to a professional. Just don’t fall for the myth that your entire salary gets taxed at the highest rate. It doesn’t.

Quick Summary

- The 2025 tax brackets divide your income into different sections.

- Only the top part of your income is taxed at the highest rate.

- State taxes are a separate system and vary widely.

- Inflation adjustments protect you from “bracket creep.”

- Use tax-advantaged accounts and credits to lower your taxable income.

Now it’s your turn: where do you fall in the 2025 tax brackets, and what’s your game plan for saving more money?

FAQs About 2025 Tax Brackets

What are tax brackets, and how do they work?

Think of it like a cake cut into slices, with each slice taxed at a different rate. Your salary works the same way, each segment of your income is taxed at a different rate. This is called a progressive tax system, where higher earners pay more, but the higher rate doesn’t apply to their entire salary.

If I’m in the 22% bracket, will my entire salary be taxed at 22%?

No! Only the income that falls into the 22% bracket is taxed at that rate. The rest of your income is taxed at the lower rates that apply to those brackets. This is a common point of confusion for many people.

What are the 2025 tax brackets for single filers?

The first $11,600 of your income is taxed at 10%. Then, the income from $11,601 to $47,150 is taxed at 12%. The remaining income levels are taxed at 22%, 24%, 32%, 35%, and 37%.

Why are the brackets different for married filing jointly or head of household?

Your tax bracket differs based on your filing status because the income ranges are set according to your specific situation. The IRS creates different categories to account for factors like family size.

How does a progressive tax system benefit me?

As your income increases, your tax rate goes up, but each smaller portion of your income is taxed at a lower rate. This prevents your entire salary from being hit with a high tax.

What’s the difference between federal and state tax?

Federal tax is a nationwide tax, while state tax varies from state to state. Some states, like Florida and Texas, have no state income tax at all.

What is the standard deduction, and what is the amount for 2025?

The standard deduction is a fixed amount that the IRS automatically subtracts from your taxable income to reduce your tax bill. For 2025, it’s $14,600 for single filers and $29,200 for those who are married and filing jointly.

What’s the difference between tax credits and tax deductions?

Deductions reduce your taxable income, but credits directly reduce your tax bill, which makes them more valuable.

What is a Health Savings Account (HSA), and what are its benefits?

An HSA is a special account where you can save tax-free money to use for health expenses. The money grows tax-free and can be withdrawn tax-free as long as it’s used for qualified health-related costs.

What are some common mistakes people make when filing their taxes?

Common mistakes include incorrect personal information, failing to report all income, missing out on deductions, filing late, not keeping proper records, and not seeking professional help.

Should I get professional help for my tax filing or use online calculators?

Both are good options. For simple tax situations, online calculators can be helpful. However, if your situation is complex, it’s better to get professional help.

Pingback: Best Debt Consolidation Loans 2025 Lower Rates, Regain Control -