Let me tell you something, I was a complete disaster with money in my twenties. Like, embarrassingly bad. I once had to borrow $30 from my roommate to buy groceries while having three different streaming subscriptions I’d forgotten about. Classic millennial move, right?

Back then, personal finance apps were either clunky or didn’t exist. I tried the whole Excel spreadsheet thing (lasted exactly two weeks), wrote budgets on napkins, and even attempted that envelope method my mom swore by. Nothing stuck. Fast forward to 2025, and we’re drowning in budgeting apps that promise to fix our financial lives. “So let’s see how true this really is.”

Here’s Why Your Last Budgeting Attempt Crashed and Burned

Before we dive into the apps, can we talk about why most budgeting attempts fail? Because I think the problem isn’t discipline – it’s using the wrong tools for your personality.

I spent years feeling guilty about “not being good with money” when really, I just hadn’t found budget tracker apps that worked with my chaotic brain. I’d download something that required me to manually categorize every $3 coffee purchase, get overwhelmed after a week, and give up entirely.

The truth is, most money management apps are built by people who are naturally organized. They assume you want to spend time analyzing spending patterns and setting up detailed categories. But what if you’re the type of person who just wants to know “am I okay to buy this thing or not?

“That’s where the app variety in 2025 actually helps. There are now budgeting apps for people who love data, people who hate numbers, people who want automation, and people who want complete control. The trick is being honest about which type you are.

Your last budgeting attempt probably failed because you picked an app that fought against your natural habits instead of working with them. Let’s fix that.

Free Budgeting Apps That Actually Work

Mint – The Old Reliable

Mint has been around forever, which in app years makes it basically ancient. But you know what? Sometimes the classics stick around for good reasons.

I used Mint for three years straight, and in my experience, it’s like that reliable friend who always remembers your birthday but isn’t the most exciting person to hang out with. It automatically connects to your bank accounts (most of them, anyway), categorizes your spending, and shows you where your money goes without much effort on your part.

The best part about Mint is that it’s completely free, and it still holds up even in 2025 when automatic budgeting apps are the big trend. Set up your categories once, and it pretty much runs itself. It’ll send you alerts when you’re close to your spending limits, which is either helpful or anxiety-inducing depending on your personality.

But here’s where Mint gets weird – the ads. Oh my god, the ads. They’ll try to sell you credit cards in the middle of showing you how much debt you have. It’s like having a financial advisor who also sells used cars.

The bank sync works about 80% of the time. That other 20% will make you want to throw your phone across the room when your transactions don’t update for three days straight. But when it works, it’s surprisingly solid for people who want a simple, ‘set it and forget it’ approach, and honestly, for a free app, those trade-offs are manageable.

Mint At Glance

- ✔️ Free forever

- ✔️ Automatic bank syncing & spending categorization

- ✔️ Good for beginners who don’t want complexity

- ❌ Ads can feel intrusive

- ❌ Occasional bank connection issues

PocketGuard – For the Overspenders

If you’re someone who sees money in their checking account and immediately thinks “shopping time,” PocketGuard might be your savior. This app has one job: tell you how much you can safely spend without screwing up your bills and savings goals.

I love PocketGuard approach because it’s so simple it almost feels dumb. Instead of showing you complicated charts, it just displays a number: “You have $247 left to spend this month.” That’s it. No analysis paralysis, no wondering if that $15 lunch fits into your “entertainment” or “food” budget.

The app connects to your bank accounts and automatically subtracts your bills and savings goals from your income. What’s left is your “In My Pocket” amount – money you can blow on whatever without guilt. It’s like having a really strict financial babysitter, which some of us honestly need.

And in 2025, when many budgeting apps still feel too complicated, the simplicity of PocketGuard number one really stands out.

The downside? If you like understanding where your money goes, PocketGuard might feel too simplified. It’s not great for detailed expense tracking or long-term financial planning. But if your main problem is impulse spending, this app will literally save you from yourself.

Goodbudget – Old School Envelope Method

Remember when your grandparents used actual envelopes to budget cash for groceries, gas, and entertainment? Goodbudget takes that concept digital, and honestly, it’s kind of brilliant for certain types of people.

Let me ask you something – do you miss the days when spending money felt more… real? When you had to physically hand over cash and watch your wallet get lighter? Goodbudget brings back some of that tangible feeling without requiring you to carry around actual envelopes.

You create virtual envelopes for different spending categories and fill them with money at the beginning of each month. When an envelope is empty, you’re done spending in that category.

It’s one of the better budgeting apps for beginners because the concept is so straightforward.

The free version gives you 10 envelopes, which is plenty for most people. The visual aspect really works – seeing your “dining out” envelope go from $200 to $30 throughout the month creates a psychological connection that spreadsheets just don’t have.

But if you hate logging every single purchase, Goodbudget will drive you crazy. There’s no automatic bank sync in the free version, so yes, you’ll need to type in each coffee run or gas stop yourself.

It works best for people who want that hands-on control, but if you’re after a ‘set it and forget it’ solution, this isn’t it.

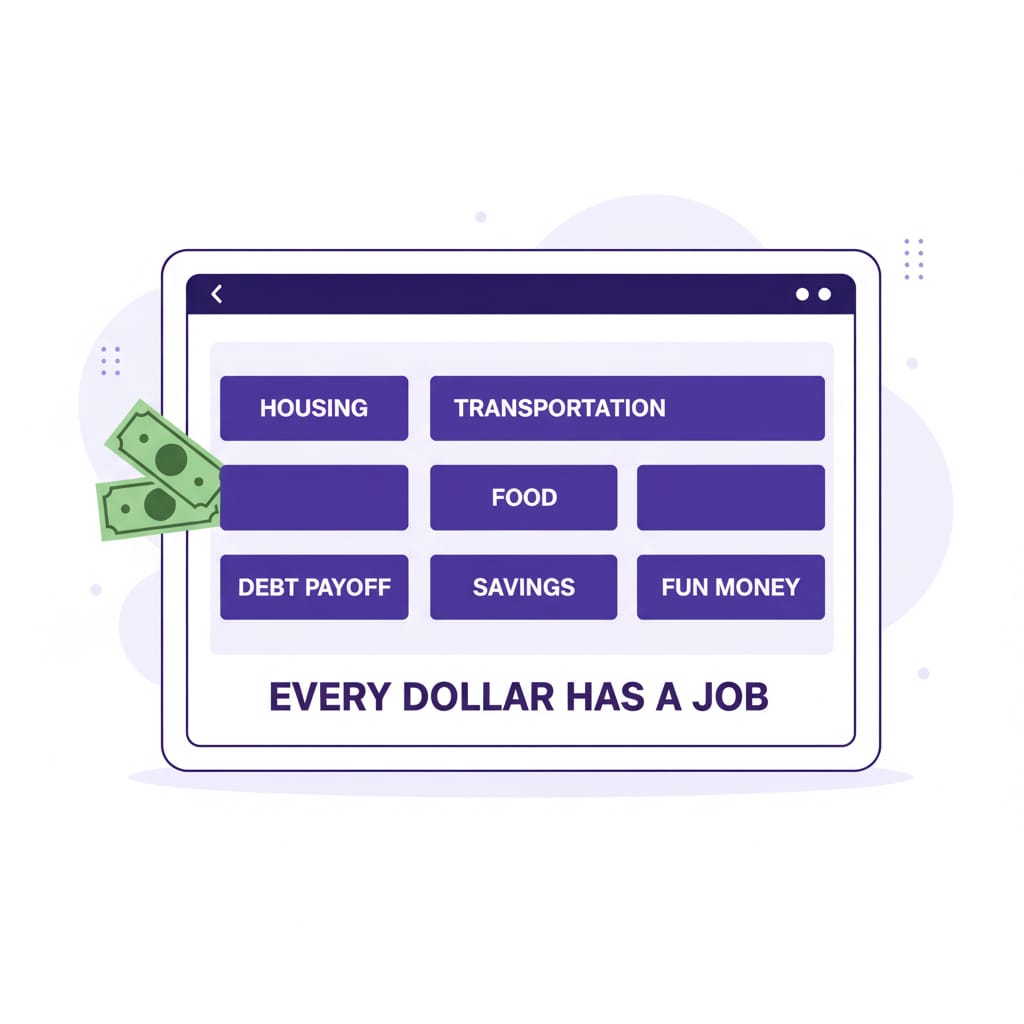

EveryDollar – Dave Ramsey’s Baby

EveryDollar comes from Dave Ramsey’s financial empire, which means it’s built around the “give every dollar a job” philosophy. If you’ve ever listened to Dave Ramsey’s radio show, you know exactly what you’re getting into.

The app pushes you to do zero-based budgeting, where your income minus your expenses should equal zero at the end of each month. Every single dollar gets assigned to a category before the month starts. It sounds intense because it kind of is.

In my experience, EveryDollar works really well for people who like having a plan and sticking to it. The interface is clean, the categories make sense, and it definitely keeps you accountable. But it’s also pretty rigid – if you’re someone whose income or expenses vary a lot month to month, the whole “plan everything in advance” approach can feel suffocating.

The free version makes you enter every transaction yourself, meditative for some, absolute torture for others. The paid plan ($17.99/month) unlocks bank syncing, but at that price, you’re up against apps that offer way more features for the money.

Even in 2025, when most budgeting apps are racing to add bells and whistles, EveryDollar keeps things old-school with its strict zero-based approach.

So then, which free app is the winner? Honestly, it depends. If you want effortless automation, Mint is best. PocketGuard acts as a guardrail for overspenders. If you like an envelope method and don’t mind a little manual work, Goodbudget is perfect. And EveryDollar? It’s the best choice for Ramsey fans who want structure.

Bottom line: The “best” app isn’t about the app, it depends on your personality.

Paid Apps Worth Your Hard-Earned Cash

YNAB – The Gold Standard (But Expensive)

You Need A Budget is like the Tesla of budgeting apps – expensive, loved by its users, and completely changes how you think about money. At $99 per year, it better be good, right?

I’ll be honest – $99 a year hurt at first, especially when I was trying to get better at budgeting. But YNAB taught me something that free apps couldn’t: how to budget money I don’t have yet. Their whole philosophy is based on only budgeting the money you currently have, which sounds obvious but is actually revolutionary for most people.

Here’s what happened when I started using YNAB: I stopped living paycheck to paycheck. Not because I was making more money, but because I was planning better. The app forces you to assign every dollar a job before you spend it, and it gets really annoying (in a good way) when you overspend in one category.

The learning curve is steep. YNAB doesn’t just track your spending – it tries to teach you a whole new relationship with money. They offer free workshops, and honestly, you’ll probably need them. It took me about two months to really “get” how YNAB works, but once it clicked, it was a gamechanger.

The best part? YNAB users are obsessed with it. Like, cult-level obsessed. There are entire Reddit communities of people sharing their YNAB success stories. When’s the last time you saw someone get excited about Mint?

The downside is obvious, it’s expensive. And if you’re not ready to completely change how you think about budgeting, you’ll probably bounce off it pretty quickly.

Tiller – For Spreadsheet Lovers

Are you one of those people who actually likes Excel? Do you get a little thrill from a perfectly formatted spreadsheet? Then Tiller might be your soulmate.

Tiller automatically pulls your transactions into Google Sheets or Excel, giving you all the power of automated bank connectivity with the flexibility of a spreadsheet. At $6.58 per month, it’s positioned as the middle ground between free apps and premium services.

I think Tiller is brilliant for people who want customization without coding. You can build exactly the budget tracking system you want, add whatever categories make sense, and create charts that actually matter to you. Plus, if you’re already comfortable with spreadsheets, there’s no learning curve.

The templates are really well done, too. They’ve got everything from basic expense tracking to complex debt payoff calculators. And because it’s all in a spreadsheet, you can modify anything that doesn’t work for your situation.

But let’s be real – if you hate spreadsheets, Tiller will be absolute torture. It’s definitely for the data nerds among us who want complete control over how their financial information is organized and displayed.

Simplifi – The Middle Ground

Simplifi is Quicken’s attempt at making a modern budgeting app, and honestly, they did a pretty good job. At $5.99 per month, it sits right between the complexity of YNAB and the simplicity of free apps.

The interface is clean without being oversimplified. You get automatic bank sync, spending insights, and bill tracking without feeling like you need a finance degree to understand what’s happening.

In my experience, Simplifi strikes a good balance between features and usability.

What I like about Simplifi is that it doesn’t try to convert you to a specific budgeting philosophy.

It just gives you tools to track your money, however makes sense to you. Want to set spending limits? Cool. Prefer to just monitor cash flow? Also cool. It’s refreshingly flexible.

The goal-setting features are solid, too. You can set up savings goals, debt payoff plans, or just track your net worth over time. The reports are useful without being overwhelming, which is harder to achieve than it sounds.

The main downside is that it’s not particularly exciting. There’s no gamification, no revolutionary approach to budgeting, no passionate user community. It’s just… competent. Sometimes that’s exactly what you need, but it might not be motivating enough if you struggle with consistency.

PocketSmith – The Crystal Ball

PocketSmith is weird in the best possible way. While most budgeting apps focus on what you’ve already spent, PocketSmith is obsessed with predicting your financial future. Their forecasting goes out 30 years, which is either incredibly useful or completely overwhelming.

The app connects to your bank accounts and uses your spending patterns to predict your cash flow months or even years in advance. Want to know if you can afford to buy a house in three years? PocketSmith will show you exactly how your current spending habits will impact that goal.

I found the forecasting genuinely helpful for big decisions. When I was considering freelancing full time, PocketSmith helped me understand how irregular income would affect my finances over time. It’s like having a financial crystal ball, assuming the crystal ball is really good at math.

The budgeting features are solid but not revolutionary. What sets PocketSmith apart is the calendar view – you can see your projected account balances for any future date, which is wild when you first experience it.

At $12.95 per month for the full version, it’s pricey. And if you’re someone who lives entirely in the present moment, all that future forecasting might just create anxiety without much benefit.

Here’s the thing about paid apps – they work better because you’re invested in them. When you’re paying $99 a year for YNAB, you’re motivated to actually use it. Free apps are easy to abandon when things get challenging. But paid apps? You’re more likely to push through the learning curve because your credit card reminds you every month.

📝 Quick Comparison: Free vs Paid Budgeting Apps (2025)

| App | Price | Best For | Main Vibe |

|---|---|---|---|

| Mint | Free | Hands-off users | Old reliable, but with ads |

| PocketGuard | Free | Overspenders | Shows what’s safe to spend |

| Goodbudget | Free (10 envelopes) | Envelope lovers | Manual entry, very old school |

| EveryDollar | Free / $17.99 mo. | Ramsey fans | Zero-based, very structured |

| YNAB | $99 / yr | Serious budgeters | Cult favorite, steep learning curve |

| Simplifi | $5.99 / mo | Most people | Balanced, clean, flexible |

| Tiller | $6.58 / mo | Spreadsheet nerds | Fully customizable sheets |

| PocketSmith | $12.95 / mo | Future planners | Forecasting + cash flow crystal ball |

Apps for Different Types of People

Look, I’ve tried probably 15 different budgeting apps over the years. Some made me want to throw my phone across the room, others actually changed how I handle money. Here’s what I’ve learned about matching apps to your actual life situation.

College Students & New Grads

Mint is still my go-to recommendation for beginners. Yeah, it’s got ads, but it’s free and connects to most US banks automatically. For my international friends, Money Lover works globally and has a decent free version.

The thing with student budgets? You need something simple that won’t overwhelm you when you’re already stressed about everything else. Don’t get fancy yet.

Young Professionals Building Their Life

Once you’ve got that first real paycheck, YNAB (You Need A Budget) becomes worth the $14/month. I know, I know – paying for a budgeting app feels weird. But trust me on this one. It actually teaches you to think ahead instead of just tracking where your money went.

Personal Capital is solid too, especially if you’re starting to invest. Free version covers most basics.

Couples & Shared Expenses

Honeydue saved my relationship, not even kidding. Shared budgets without the awkward money fights. You can see each other’s spending without being controlling about it.

For roommates, Splitwise handles all those “who paid for groceries” moments that turn friends into enemies.

Side Hustlers & Freelancers

Tiller connects to Google Sheets – perfect if you’re already living in spreadsheets for your business. QuickBooks Self-Employed gets expensive but handles taxes automatically, which is honestly worth it during tax season.

Quick Comparison

| App | Best For | Key Feature | Cost | Global Access | Ease of Use |

|---|---|---|---|---|---|

| Mint | Beginners | Auto-categorization | Free | Mostly US | ✅ Easy |

| YNAB | Serious budgeters | Forward planning | Paid – $14/month (34-day trial) | Yes | ⚠️ Steeper learning |

| Honeydue | Couples | Shared accounts | Free | US/Canada | ✅ Simple |

| Personal Capital | Investors | Net worth tracking | Free | US only | ✅ Easy |

| Money Lover | International users | Multi-currency support | Free / Premium plans | Worldwide | ✅ Easy |

| Tiller | Spreadsheet lovers | Google Sheets integration | Paid – $6.58/month (30-day trial) | US only | ⚠️ Requires setup |

Bottom Line

Don’t overcomplicate this. Pick one app, use it for 3 months consistently, then decide if it’s working. The best budgeting app is the one you actually open regularly.

What matters more than the app itself? Actually looking at your numbers instead of avoiding them. Trust me, I learned this the hard way.

The Brutal Truth About App Switching

Why You’ll Probably Try Three Apps Before Finding ‘The One’

Let me tell you about my budgeting app graveyard. I’ve got probably twenty different apps installed on my phone from various attempts to find the “perfect” budgeting solution. Mint lasted eight months. YNAB was great for two years until I got lazy about entering transactions. I tried Goodbudget for exactly three weeks before the manual entry drove me crazy.

I think this is totally normal, and here’s why, your relationship with money changes over time. The app that worked great when you were just trying to stop overdrafting might not be the same one you need when you’re saving for a house or managing a family budget.

App switching isn’t a sign of failure. It’s actually a sign that you’re learning what works for you. Each app teaches you something about your money habits, even if you eventually move on to something else.

The key is not to see app switching as starting over. Your budgeting journey is cumulative, every app you try builds your understanding of personal finance, even if the app itself doesn’t stick around.

Here’s what I’ve learned from all that app switching: the best budgeting app is the one you’ll actually use consistently for at least six months. Not the one with the most features, not the one with the best reviews, but the one that fits into your life without requiring you to become a different person.

Some people find their forever app on the first try. Others go through five or six before finding the right fit. Both paths are completely fine. The important thing is that you keep trying instead of giving up on budgeting altogether just because one app didn’t work out.

If I Had to Choose Right Now…

I’m currently using YNAB for my main budgeting and PocketSmith for long-term planning. Yes, I’m paying for two apps, which probably sounds ridiculous. But here’s the thing – YNAB keeps me on track day-to-day, and PocketSmith helps me make big financial decisions by showing me the long-term impacts.

If I could only pick one? Probably YNAB, but that’s because I’m at a place in my life where I want active budgeting rather than passive tracking. Three years ago, I would have said Mint because I just wanted something simple that worked automatically.

But that’s just me, you might be totally different. If you hate the idea of assigning every dollar a job, YNAB will drive you crazy. If you love data and customization, Tiller might be perfect. If you just want to stop overspending without thinking about it too much, PocketGuard could be your answer.

The best budgeting app is the one that matches where you are right now, not where you think you should be. Be honest about your habits, your goals, and how much time you actually want to spend managing your budget. Then pick accordingly.

Here’s What I Wish Someone Told Me at 22

After trying every major budgeting app available in 2025, here’s what I’ve learned: the app doesn’t matter nearly as much as you think it does.

I spent years thinking I was bad with money because I couldn’t make budgeting spreadsheets work. Then I thought I just needed the right app to fix everything. The truth is, personal finance apps are just tools – they can make good financial habits easier, but they can’t create those habits for you.

The best budgeting app is the one you’ll actually use six months from now when the novelty has worn off and budgeting feels like a chore. It’s not the one with the most features or the prettiest interface or the most aggressive marketing budget. It’s the one that feels natural enough that you don’t have to force yourself to open it.

FAQs

What’s the best free budgeting app in 2025?

Honestly, it depends on your style. Mint is great if you like “set it and forget it.” PocketGuard works best if you overspend easily, while Goodbudget is perfect for the envelope method fans.

Is YNAB really worth paying for?

Yep, if you’re serious about changing how you think about money. At $99/year, it’s not cheap, but most users swear it’s a total game-changer for breaking the paycheck-to-paycheck cycle.

Which budgeting app is best for couples?

If both of you are equally committed, YNAB is the winner—it lets you share real-time updates. But if you want something less intense, Simplifi is a great middle ground.

Can I track both personal and side hustle money in one app?

Totally. Tiller is amazing for this because you can separate sheets for business and personal, but still see the big picture in one place.

Should I start with a free app or go straight to paid?

Start free. If you stick with it for a few months and feel limited, that’s your signal to upgrade. A free app you actually use beats a paid one you ignore.