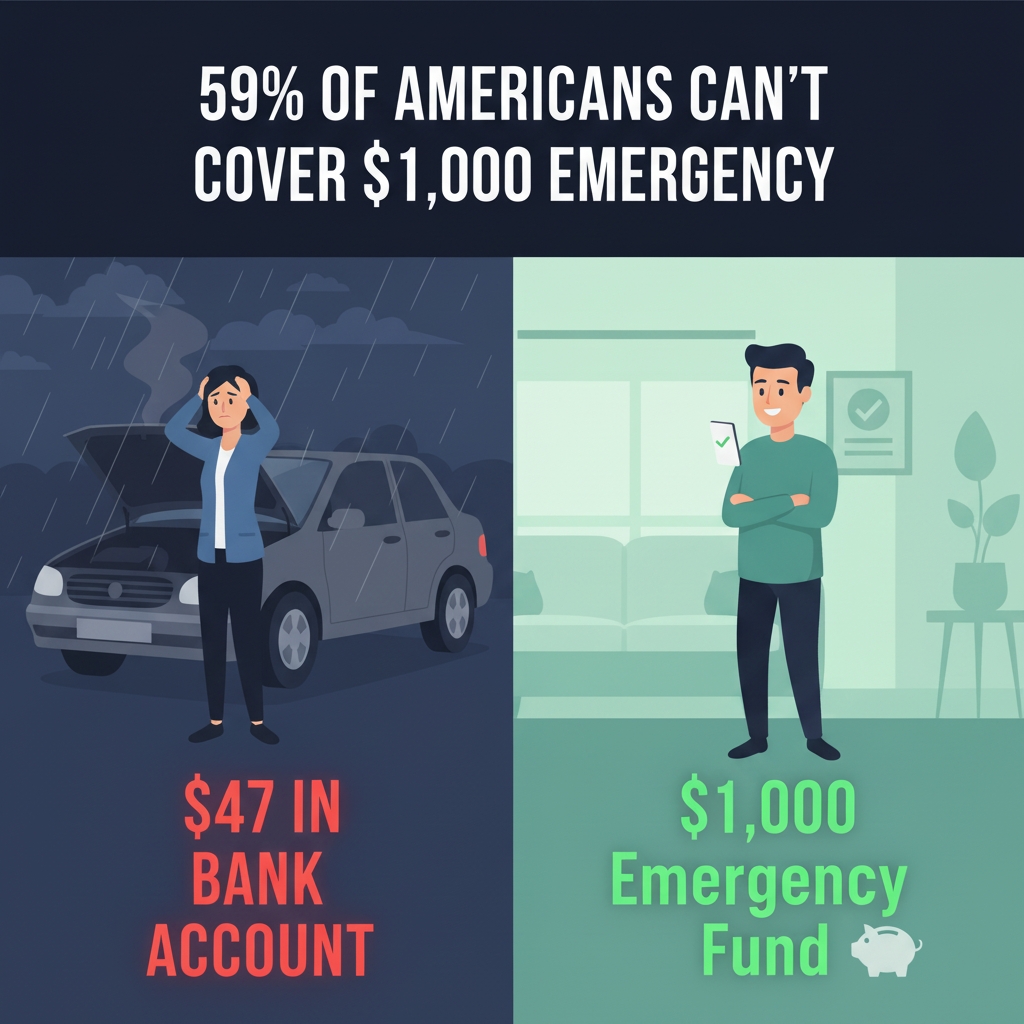

This happened a few months ago. My friend Annie called me around 10 or 11 at night and said, “Miles, I’m stuck on the highway, my car broke down, and the tow truck guy wants $200. But I only have $47 left in my checking account. Please help me.” (So yeah, I helped her.)

But that night made me realize just how important an emergency fund really is. And what I learned, I want to share with you today.

Here’s the thing no one tells you: building an emergency fund isn’t just about money. It’s about psychology, timing, and a little bit of controlled panic.

The Reality Check Nobody Mentions

I’m going to be brutally honest here. Most “emergency fund for beginners” advice makes me want to throw my laptop out the window.

“Save $50 a month and in two years you’ll have $1,200!”

Great. What happens when your transmission dies next Tuesday?

The traditional emergency fund rule of thumb says you need 3-6 months of expenses. That’s anywhere from $9,000 to $18,000 for most people. At $50 a month, you’re looking at 15-30 years. Seriously? Who has that kind of time when emergencies don’t wait for your savings timeline?

Emergency Fund Targets

| Monthly Expenses | 3-Month Fund | 6-Month Fund | “Fast Start” Goal |

|---|---|---|---|

| $2,500 | $7,500 | $15,000 | $1,000 |

| $3,500 | $10,500 | $21,000 | $1,000 |

| $4,500 | $13,500 | $27,000 | $1,000 |

I think the whole approach is backwards. Instead of asking “How much should I save monthly?”

we should be asking “How fast can I get to a minimum safety net?”

Because here’s what I’ve learned: $1,000 in the bank changes everything. Not financially, psychologically. It’s the difference between panic and inconvenience.

Quick Self-Assessment: Right now, if your car needed a $500 repair tomorrow, would you sleep tonight? If the answer is no, then traditional advice isn’t moving fast enough for you.

The Psychology Behind Speed (And Why Your Age Actually Matters)

OKAY..Let me switch gears here and discuss something unusual I’ve noticed.

People who are desperate to build an emergency fund actually do it faster than people who are just “being responsible.”

Check Out These Numbers That Blew My Mind

| Generation | % Uncomfortable | Average Emergency Fund |

|---|---|---|

| Gen Z (18–28) | 29% | 💵 ~ $9,459 |

| Millennials (29–44) | 40% | 💵 ~ $15,000 |

| Gen X (45–60) | 31% | 💵 ~ $25,000 |

| Baby Boomers (61–79) | 52% | 💵 ~ $35,000 |

See that? Gen Z actually feels the most confident about their savings, even though they have the least. Know why? Because they’re in crisis mode. They’re learning how to build an emergency fund fast out of necessity.

Why does desperation work? Because it creates focus. When you’ve been burned by a financial emergency, your brain doesn’t want to experience that helplessness again. That’s pure, usable motivation right there.

I remember when I first started trying to figure out how to build an emergency fund fast. I’d just gotten hit with a $1,200 dental bill (root canal – fun times), and I was done feeling financially vulnerable.

That desperation? It made me creative. It made me hustle. It made me question every dollar I spent.

Your brain on a financial emergency is different from your brain reading personal finance blogs on a Sunday afternoon. Use that energy.

The momentum effect is real too. Once you see your emergency fund balance hit $100, then $300, then $500 – something clicks. You start protecting that number like it’s your firstborn child.

But here’s the catch: this motivation has an expiration date. Most people hit a wall around 6-8 weeks. We’ll talk about that later.

Fast-Track Strategies That Actually Work

Alright, let’s get into the meat of this. The best emergency fund strategies aren’t about optimizing your coffee budget, they’re about finding money you forgot you had and creating new income streams fast.

Immediate Wins (0-30 Days)

Sell stuff you forgot you owned. I’m serious. Right now, go look in your closet, garage, or that drawer where electronics go to die.

Last year, I helped my neighbor clean out her spare room. We found a bread maker still in the box ($89 on Facebook Marketplace), a set of golf clubs from her ex-husband ($180), and three phone cases for phones she didn’t even own anymore ($15 each).

Total: $314 in three hours. Not bad for a Saturday morning.

The reality check on side hustles. Everyone talks about DoorDash and Uber, but let me tell you what actually works fast: skills you already have.

Can you edit documents? Upwork. Can you organize spaces? TaskRabbit. Can you explain math to high schoolers? Wyzant.

The emergency fund tips for young adults always mention gig work, but they miss the point. You don’t need to learn new skills – you need to monetize existing ones quickly.

Medium-Term Moves (1-3 Months)

Income optimization that doesn’t require a new job. Ask for overtime. Pick up extra shifts. If you’re salaried, see if there are project bonuses available.

I know a teacher who makes an extra $200 a month grading standardized tests from home. Two hours a week. That’s $2,400 a year straight into her emergency fund.

The expense audit nobody wants to do. Here’s where I’m going to make you uncomfortable.

Track everything for one week. Not to judge yourself, but to see where your money actually goes versus where you think it goes. If you need a complete system for this, check out our guide on how to create a personal budget that actually works in 2025.

Most people discover they’re spending $40-60 a month on subscriptions they forgot about.

That’s $480-720 a year. Boom – there’s a chunk of your emergency fund target amount right there.

Automation like your life depends on it. Because honestly? It might.

Set up automatic transfers for every bit of extra money. Tax refund? Straight to emergency fund. Work bonus? Emergency fund. Found $20 in your jeans? Okay, maybe keep that one, but you get the idea.

What’s your biggest money leak right now? The thing you spend on without thinking? That’s your starting point.

Acceleration Tactics (Ongoing)

The fastest way to build wealth isn’t making more money, it’s plugging the holes in your financial boat.

But sometimes you need to do both.

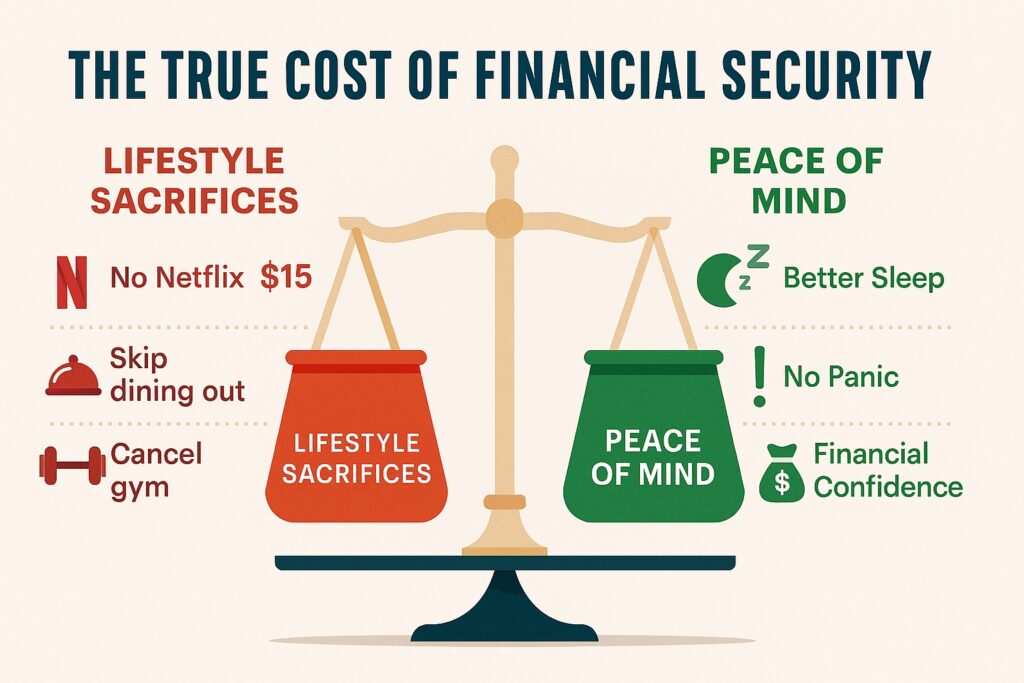

The Uncomfortable Truth About Sacrifices

Here’s where most articles get wishy-washy. Not this one.

If you want to know how to build an emergency fund fast, you’re going to give up stuff. Probably stuff you like.

For three months, I ate lunch at home every single day. Not because I’m some financial guru, but because $12 a day is $240 a month. That’s $720 in three months, enough for most car repairs.

Was it fun? No. Did it work? Absolutely.

The social pressure is real, too. Your friends are going to notice when you stop joining every dinner out, every concert, every “quick drink” that turns into a $60 tab.

Some people will say, “Wow, Annie’s being so cheap. What’s she even going to do with that money?”

But I think Annie sleeps a lot better with $2,000 in her bank account than she ever did when she only had $47.

Here’s the thing though, cutting expenses doesn’t have to make you miserable. If you’re worried about feeling deprived while building your emergency fund, I’ve written extensively about how to save money fast without feeling like you’re missing out. The key is finding smart substitutions, not just eliminating everything fun.

Your lifestyle might need a reality check. I’m not saying become a hermit, but I am saying that building an emergency fund fast requires temporary discomfort for long-term peace of mind.

When I was laser-focused on building my fund, I cancelled Netflix, Spotify, and my gym membership for four months. Used the library for entertainment and ran outside. Saved $89 a month.

Did I miss The Office reruns? Sure. But I didn’t miss the panic when my water heater died.

Where to Stash It (Plot Twist Alert)

Okay, unexpected topic change here, but this matters more than you think.

The whole emergency fund vs savings account debate is usually pretty straightforward. High-yield savings, credit union accounts, money market funds, all solid choices.

But here’s my controversial take: accessibility matters more than yield when you’re starting out.

I know, I know. Everyone says get the highest interest rate possible. But when you’re learning how to build an emergency fund fast, the goal is building the habit and seeing progress.

If your emergency fund is in some online bank that takes three days to transfer money, are you really going to use it in an emergency? Or are you going to put that car repair on a credit card because it’s faster?

Start with whatever account lets you see the balance growing daily. Once you hit $2,000, then optimize for yield.

Best Emergency Fund Accounts (2025)

💰 Popular High-Yield Savings Options (Rates as of September 2025)

| Bank / Institution | Approx APY | Notes |

|---|---|---|

| Marcus by Goldman Sachs | 3.65% | Verify current rates at marcus.com |

| Ally Bank | ~3.60% | Online high-yield savings. ally.com |

| American Express | ~3.50% | High-yield savings account. americanexpress.com |

| Synchrony Bank | ~3.80% | Rates may vary with promotions. synchronybank.com |

Disclaimer: Interest rates change frequently. Always verify current rates directly with each institution before making decisions. This information is for educational purposes only.

My first emergency fund lived in a basic savings account at my main bank. Could I have earned an extra $15 a year somewhere else? Sure. Did seeing that number grow every week keep me motivated? Absolutely.

Quick action step: Open whatever account you can fund today. Perfection is the enemy of progress.

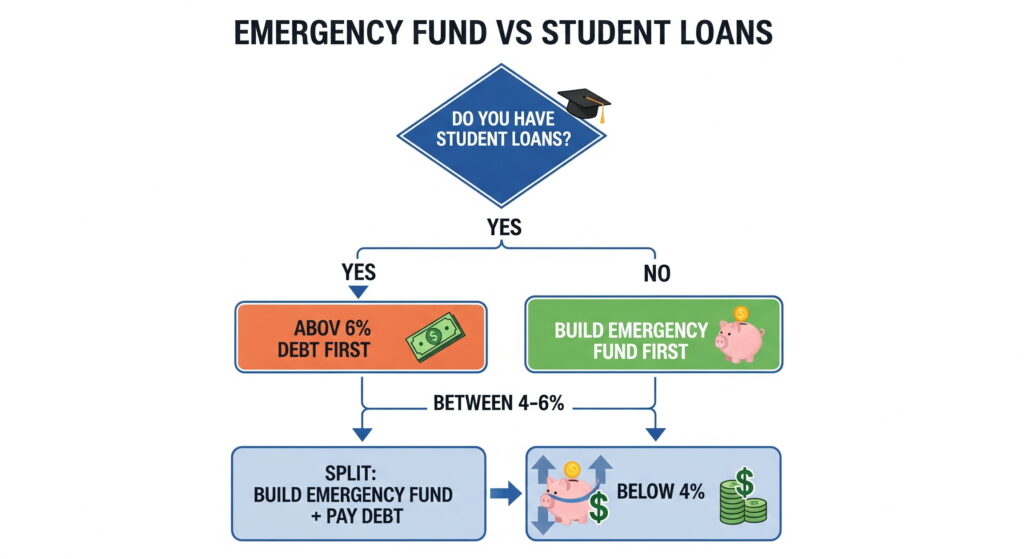

The Student Loan Dilemma (Because I Know You’re Wondering)

Real quick, I know what some of you are thinking. “But what about my student loans? Should I pay those off first?”

This is where things get personal. If you’re drowning in high-interest student debt, you might need a different approach altogether. I’ve covered this exact dilemma in detail in our complete guide to getting out of student loan debt, but here’s the short version:

If your student loan interest rate is above 6%, prioritize that debt while building a small $1,000 emergency buffer. If it’s below 4%, build the emergency fund first.

But honestly? Having both debt and zero emergency savings is a recipe for more debt. Better to have $1,000 in the bank and a student loan payment than no savings and a bigger student loan balance after the next emergency.

Staying Motivated When It Gets Hard

I mentioned earlier that motivation has an expiration date. Let me tell you about the 6-week wall.

🚧 The 6-Week Wall

- Week 1-2: You’re excited. This emergency fund thing is happening!

- Week 3-4: Still good. You’re seeing progress.

- Week 5-6: This is boring. The balance is growing slowly. Netflix is calling.

- Week 7+: Danger zone. This is where most people quit.

I’ve seen it happen to so many people. The novelty wears off, progress feels slow, and suddenly that emergency fund savings plan starts gathering dust.

🎉 How to Push Through

Here’s what actually works to push through: celebrate small wins obnoxiously.

- Hit $250? Tell someone. Take a screenshot. Do a little dance. I’m serious.

- Hit $500? That’s a major car repair covered. Celebrate bigger.

- $1,000? That’s “I can sleep at night” money. That deserves recognition.

The goal isn’t just building the fund, it’s rewiring your brain to value financial security over instant gratification.

Track your progress somewhere visible. I used a simple spreadsheet, but some people love those savings thermometer printables. Whatever works for you.

And be honest about setbacks. I had to use my emergency fund twice while building it. First time, I was devastated. Second time, I was grateful I had it. That’s the whole point.

The Good News Stats: Want some encouragement? 30% of Americans actually increased their emergency savings in 2024, according to Bankrate. And get this – 55% now have three or more months of expenses saved.

So yeah, people are figuring this out. You can too.

In my experience, the people who successfully build emergency funds fast are the ones who treat it like a game with levels to unlock, not a boring responsibility to slog through.

Your 90-Day Challenge

Alright, let’s wrap this up with some real talk and specific next steps.

Most emergency fund calculators will tell you that you need $15,000 and it’ll take you five years to save it. That’s not wrong, but it’s not the whole story either.

Here’s what I think: $1,000 in 90 days is better than $15,000 in five years. Not mathematically, but practically.

$1,000 covers most smaller emergencies. More importantly, it proves to yourself that you can do this.

Your next steps:

- Day 1: Open the account. Today. Not tomorrow.

- Week 1: Sell three things you don’t need.

- Week 2: Set up automatic transfers, even if it’s just $25 a

- Week. Week 4: Audit your subscriptions and recurring expenses.

- Week 8: Look for ways to increase income temporarily.

- Week 12: Celebrate hitting your first milestone.

The internet is full of people promising you can build a six-month emergency fund in six weeks. That’s usually unrealistic unless you’re already making six figures.

But $1,000 in 90 days? If you’re reading this article, you can probably do it.

Will it require sacrifices? Yes. Will some people think you’re being extreme? Maybe. Will you sleep better at night? Definitely.

The best emergency fund strategies aren’t about perfection, they’re about progress. And progress starts today, not when your budget is perfect or when you get that raise or when life gets less complicated.

Life doesn’t wait for you to be financially ready. But you can get financially ready for life.

Your future self, standing in that auto repair shop without panic in their chest, will thank you for starting today.

Now stop reading and go open that account.

One Final Reality Check:

Real numbers show that building an emergency fund isn’t just a good habit, it’s a necessity.

- A CNBC survey found that 56% of Americans can’t cover a $1,000 emergency from their savings.

- Another survey shows that 42% of people have no emergency savings at all, and 40% wouldn’t be able to handle a $1,000 surprise expense in cash.

- According to NerdWallet’s 2023 Savings Report, only 45% of people have enough saved to cover a $1,000 emergency. The report also highlights how people rely on debt, offering an eye-opening look at current saving habits.

- Even common car repairs can be expensive. Kelley Blue Book reports that replacing an alternator typically costs $750–$850, and brake pads and rotors cost $550–$650.

FAQ’S

How much ought I to have saved?

Aim for about three to six months’ worth of expenses, such as rent, food, utilities, transportation, and insurance; if you spend $4,000 a month, that comes to $12,000 to $24,000; if you are self-employed, have a variable income, or only get one paycheck, go for the higher end (6–12 months) so you can sleep easy.

How can I construct one?

Begin modestly. Even if it’s only $25 to $50 per month, set up an automatic transfer from your checking account. Consider it a self-imposed bill. To expedite the process, include any additional funds you receive, such as bonuses, tax returns, or gift money. The goal is to continue, not to save everything at once.

Where ought the funds to go?

Place it in a separate high-yield savings account that’s easy to access but not so easy that you’ll dip into it for random stuff.

Skip stocks, crypto, or retirement accounts, you don’t want to risk losing money right when you need it.

When should I use it?

Only for real emergencies, like:

Losing your job or a big chunk of income

Major medical bills that insurance doesn’t cover

Essential home or car repairs

Family emergencies that require travel

Don’t use it for vacations, sales, new gadgets, or “I just felt like it” expenses.

What if I have to use it?

Refill it as soon as you can.

Cut back on extras for a bit, set a goal to get at least $1,000 saved within a month, then work back up to your full target.

Side gigs or selling stuff you don’t use can help too.

What mistakes should I avoid?

Treating it like an investment account

Spending it on non-emergencies

Keeping it in an account that earns almost nothing

Mixing it with regular spending money

Stopping contributions once you hit your goal, life changes, so keep adjusting

Should I save first or pay off debt?

Do both, but in the right order:

Save a small starter fund (about $1,000) so you don’t rely on credit cards for every surprise.

Then tackle your high-interest debt.

Once that’s gone, build up your full emergency fund.