Picture this: You’re 25, fresh out of college, and you just found the perfect apartment. The rent is fair, the location is great, everything feels right, until the landlord asks for your credit score.

Suddenly you’re left wondering: “Wait… what even is a credit score? How to build & repair your credit if paying rent or phone bills doesn’t count?”

I’ve been there. Most people starting out in the U.S. have been there too. The truth is, your credit score isn’t just a random number, it’s your financial reputation in digits. And in the U.S., this little three-digit number controls way more of your life than you probably realize.

Before we dive into how to build & repair your credit, let’s look at one surprising gap that affects millions of renters in the U.S.

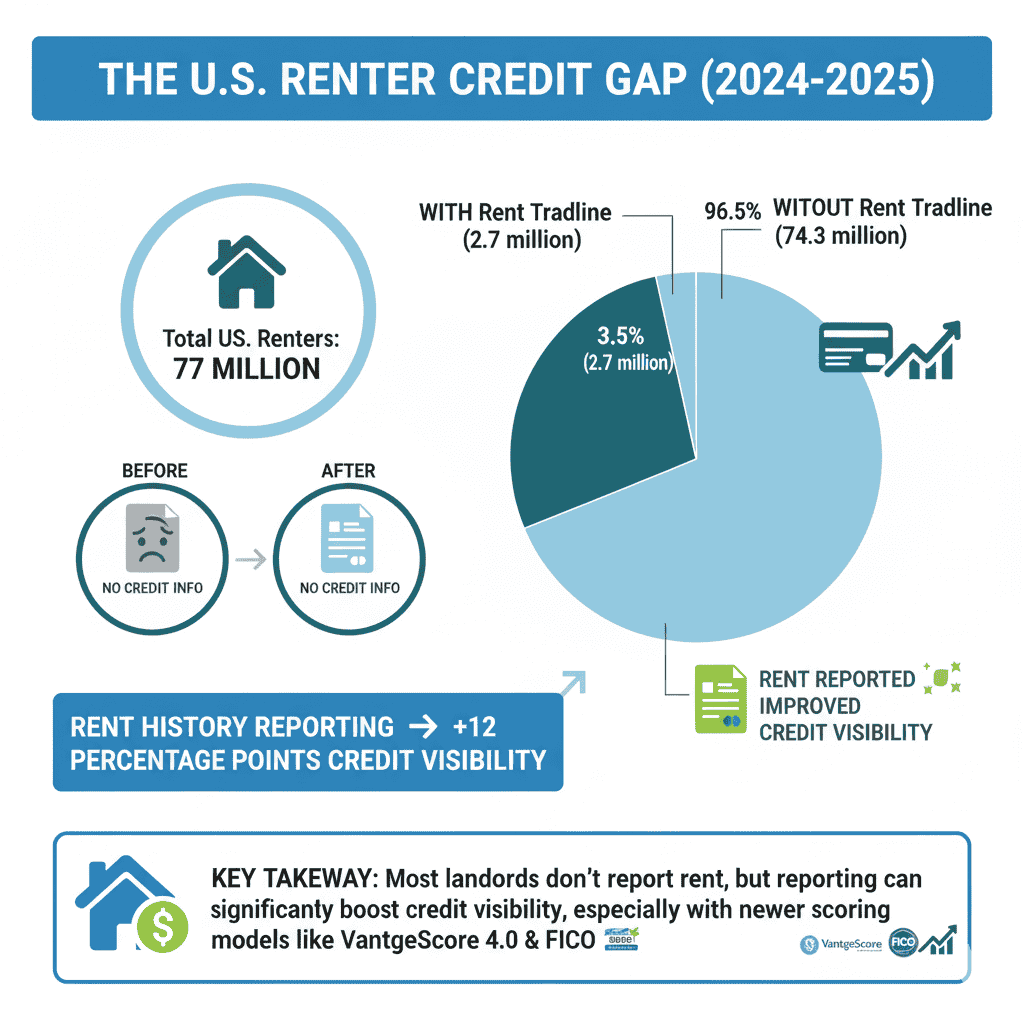

The Credit Gap: Why Paying Rent Doesn’t Always Build Credit (2024–2025)

Here’s a surprising fact: as of 2024, only about 2.7 million renters, just 3.5% of the 77 million renters in the U.S. have at least one rent tradeline showing on their credit report Urban Institute, 2025

On the flip side, a randomized trial in 2021-2022 showed that when rent history is reported, renters with thin or no credit files saw their credit visibility jump by 12 percentage points, and many improved into the “near-prime” score range Urban Institute study via NLIHC

The short answer is: not automatically. Most landlords don’t report rent payments, and credit bureaus won’t see them unless you or your property manager use a rent-reporting service Experian

But when rent is reported, studies consistently show meaningful improvements in credit scores and visibility NLIHC, 2022). Plus, newer scoring models like VantageScore 4.0 and some FICO versions are starting to include rental and utility data when it’s available Investopedia, 2025

What is a Credit Score? (The Basics)

Alright, let’s start simple. A credit score is essentially a three-digit number that ranges from 300 to 850. Think of it as your financial GPA – except this one actually matters after graduation.

The average credit score in February 2025 was 715, which puts things in perspective. If you’re sitting around 650, you’re not doomed. If you’re at 750, you’re doing pretty well.

📊 Credit Score Range Guide

| Credit Score Range | Category | Meaning / Consequence |

|---|---|---|

| 300 – 579 | Poor | Hard to get approval, very high interest rates |

| 580 – 669 | Fair | Approval possible, but higher risk and higher rates |

| 670 – 739 | Good | Generally approved for credit |

| 740 – 799 | Very Good | Strong rating, access to better terms |

| 800 – 850 | Excellent | Top score, lowest interest rates available |

But here’s where it gets interesting (and where most people get confused): there are different types of credit checks, and understanding them can save you from accidentally tanking your score.

Soft vs Hard Inquiries Explained

Let me break this down because this trips up SO many people.

A soft credit check is like someone peeking through your window – they can see what’s going on, but they don’t leave any footprints. When you check your own credit score, when a credit card company pre-qualifies you, or when a potential employer runs a background check – that’s a soft pull credit check.

A hard inquiry is different. This is like someone walking through your front door and leaving muddy footprints on your carpet. When you apply for a credit card, auto loan, or mortgage, that’s a hard credit check. And yeah, it dings your score a few points.

Here’s the kicker: the difference between soft credit check vs hard credit check isn’t just about the impact on your score. It’s about intention. Hard inquiry vs soft inquiry comes down to this – are you actively seeking credit (hard) or just monitoring/being evaluated (soft)?

I think the biggest mistake people make is avoiding soft inquiry checks because they’re scared it’ll hurt their credit. Nope! Check your score monthly. Use those free tools. Get pre-qualified. Soft credit checks are your friends.

🔍 Soft Inquiry Vs. Hard Inquiry: What’s the Difference?

| Aspect | Soft Inquiry | Hard Inquiry |

|---|---|---|

| Effect on Credit Score | No impact | Small temporary drop (around 5–10 points) |

| When It Happens | Checking your own credit, pre-qualification, background checks | Applying for a loan, credit card, or mortgage |

| Your Permission | Not always required | Always required |

| Visibility | Only visible to you | Visible to all lenders |

| How Long It Stays | About 2 years (but no score impact) | About 2 years (and does affect your score) |

| Examples | Viewing your credit score, receiving pre-approved offers, employer background check | Applying for a credit card, car loan, personal loan, mortgage |

Quick tip: Use Credit Karma or your bank’s free credit monitoring for regular soft pulls. Credit Karma remains one of the best free options, though Experian is rated best overall for comprehensive monitoring.

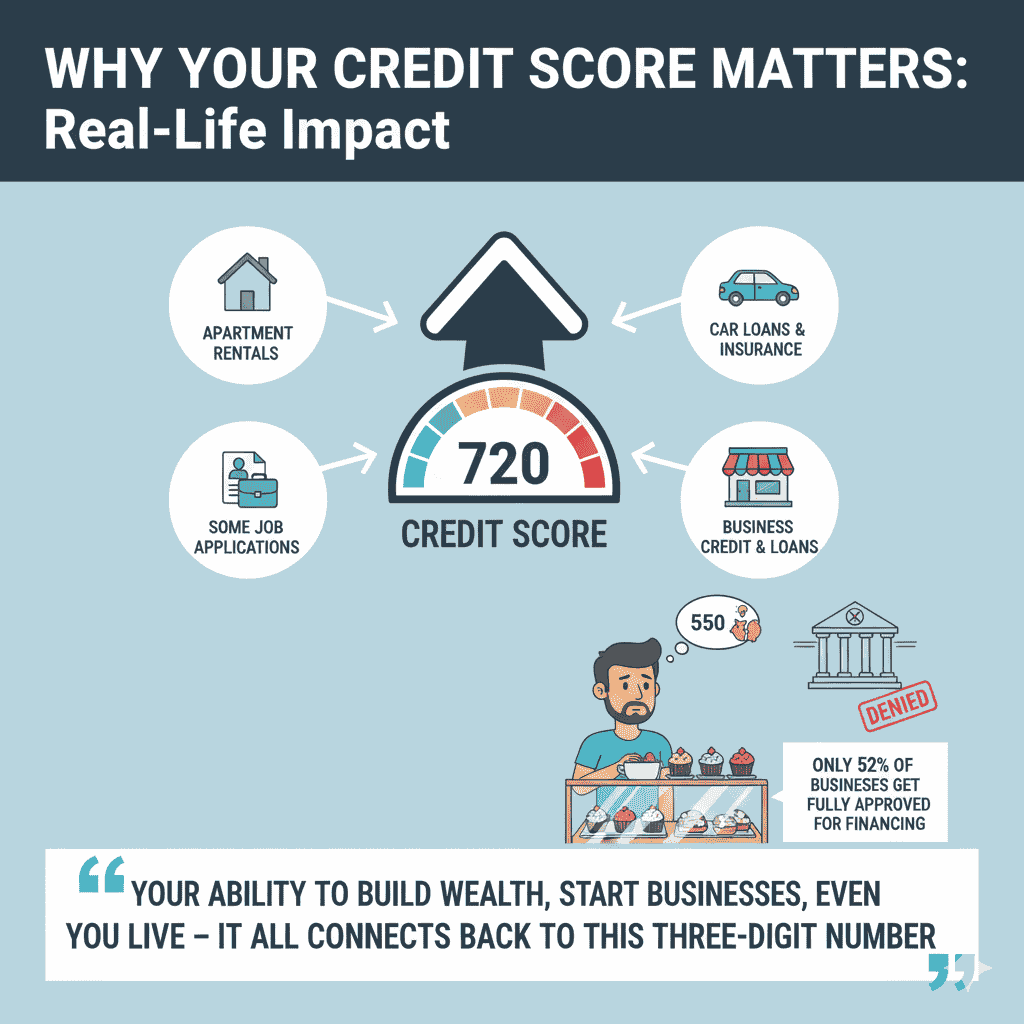

Why Credit Scores Matter in the USA

Here’s where credit scores get real. And honestly, sometimes annoyingly powerful.

Your credit score affects:

- Apartment rentals (and here’s where “does paying rent help credit” becomes relevant)

- Car loans and insurance rates

- Business credit opportunities

- Even some job applications

But here’s what’s wild – while your rent payments might not automatically build credit, landlords absolutely use your credit score to decide if you’re worthy of their property. The irony is thick.

I remember talking to my friend, who wanted to start a small business. She had this brilliant idea for a local bakery, stable income, great business plan. But her personal credit score was blocking her access to business credit options.

This is crucial: only 52% of businesses get fully approved for financing they apply for. And often, it comes down to the owner’s personal credit score.

Think about that for a second. Your ability to build wealth, start businesses, even where you live – it all connects back to this three-digit number.

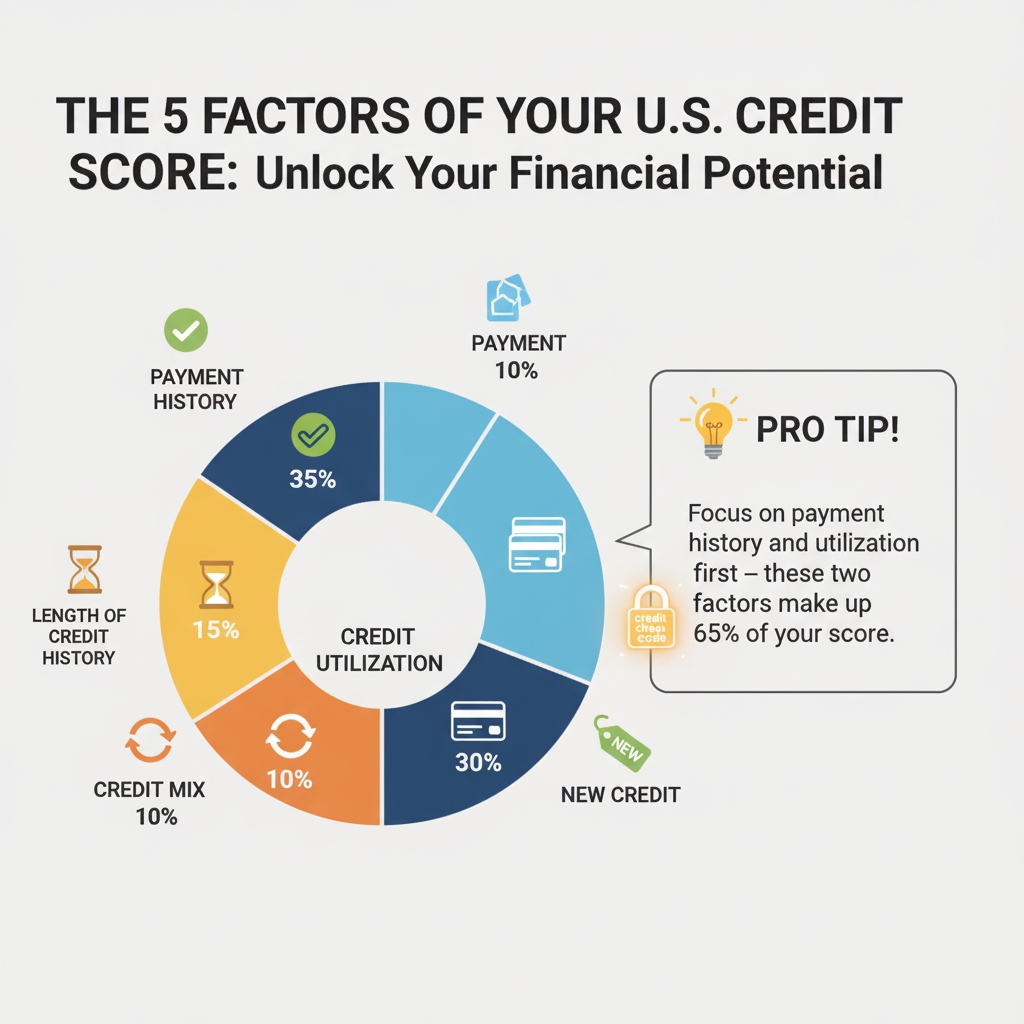

What Makes Up Your Credit Score?

Your credit score isn’t random. It’s calculated based on five main factors, and understanding these is like getting the cheat codes to the game.

- Payment History (35%) – This is the big one. Pay your bills on time. Every time. Late payments are credit score killers.

- Credit Utilization (30%) – Keep your credit card balances low. Ideally under 30% of your limit, but under 10% is even better.

- Length of Credit History (15%) – This is why closing old credit cards can hurt. Keep those accounts open.

- Credit Mix (10%) – Having different types of credit (cards, loans, etc.) shows you can handle variety.

- New Credit (10%) – Don’t apply for multiple credit cards in a short period.

Here’s a pro tip that connects to our earlier discussion: you can pay bills build credit if you’re strategic about it. While your regular utility payments might not automatically report to credit bureaus, there are ways to make them count. More on that in a bit.

The thing is, most people obsess over the wrong factors. They’ll stress about credit mix while carrying high balances. Focus on payment history and utilization first – those two factors alone make up 65% of your score.

How to Build Credit from Scratch (Beginners & Newcomers)

Starting from zero credit feels a lot like trying to land a job when every employer wants “experience.” Frustrating, right? The good news is, there are proven ways to get started.

1. Use a Secured Credit Card

Think of this as training wheels for your credit journey. You put down a deposit (say $200), and that becomes your credit limit. Use it for small purchases, pay it off completely every month, and you’ll slowly start building a positive history.

2. Become an Authorized User

If you have a parent, spouse, or close friend with solid credit habits, ask if they’ll add you as an authorized user on their card. Their good payment history can give your score a nice boost. Just make sure you trust them, if they slip up, it could affect you too.

3. Try Student or Newcomer Credit Cards

Students often qualify for starter credit cards designed specifically for people with little to no history. If you’re new to the U.S., some banks even offer credit cards for immigrants to help you get established faster.

Rent & Utility Reporting: A Game Changer for Your Credit Score

Remember when I asked if paying rent helps your credit? The real answer is: yes, but only if it’s actually reported.

Here’s why this matters:

The average credit score increase from rent reporting is 23 points. That could literally move you from “declined” to “approved.”

How Rent Reporting Works

Normally, rent payments don’t show up on your credit file. But services like RentReporter, Rental Kharma, and others step in to report your on-time payments directly to the credit bureaus. Some are free, some charge a small fee, but all can make a big difference.

Big players are noticing too:

- Fannie Mae is covering rent reporting costs through June 30, 2025, for some renters.

- NYC launched a rent reporting pilot in September 2025.

- This shows rent reporting is quickly becoming mainstream.

What About Utility Bills?

Good news, some services now report utilities as well. The most popular is Experian Boost, which is completely free. You simply connect your bank account, it finds qualifying payments (utilities, phone, even streaming services), and adds them to your credit file.

🏠 Rent & Utility Reporting Services

| Service | Cost | What It Reports | Reports To |

|---|---|---|---|

| Experian Boost | Free | Utilities, phone, streaming, rent | Experian only |

| RentReporter | Paid | Rent payments only | Experian, TransUnion |

| PayYourRent | Varies (landlord-based) | Rent (if landlord participates) | Experian, Equifax, TransUnion |

| Rental Kharma | Paid | Rent payments (comprehensive) | TransUnion, Equifax |

If you want an instant boost, start with Experian Boost. It’s free, takes about 10 minutes, and can raise your score using bills you’re already paying.

How to Repair & Rebuild Bad Credit

Let’s be real! sometimes credit just gets messy. Job loss, medical bills, divorce, or maybe just bad money choices in your twenties. It happens.

The good news? Fixing your credit isn’t some mysterious process that only expensive “credit repair” companies understand. Most of it, you can do yourself. Here’s how:

Step 1: Pull Your Free Credit Reports

Go to annualcreditreport.com and grab your reports from all three bureaus. Check carefully, chances are, you’ll find at least one error. Common ones include wrong payment history, mixed-up files, or even accounts opened through identity theft.

Step 2: Dispute Errors in Writing

If you spot a mistake, don’t just shrug it off. Write to the credit bureaus directly, they legally have 30 days to investigate and get back to you. (Pro tip: send it by certified mail so you have proof they received it.)

Step 3: Pay Down High Balances

Your credit utilization ratio has a massive impact on your score. Knocking down those balances is one of the fastest ways to see improvement. Even paying a little extra each month makes a difference.

If high balances are weighing you down, consider exploring debt consolidation loans with lower rates. They can help you simplify payments, reduce interest costs, and make the path to repairing your credit much smoother.

Step 4: Keep Old Accounts Open

Don’t rush to close old cards, even if you’re not using them. The longer your credit history, the better your score looks. Those old accounts are basically your “track record.”

Step 5: Automate Your Payments

Payment history makes up 35% of your score, the single biggest factor. Setting up autopay means you’ll never miss a due date (and avoid the 50–100 point drop one late payment can cause).

Here’s something I learned the hard way: paying off collections doesn’t always give your score an immediate bump. Sometimes, it even dips a little at first. Don’t panic, the scoring models are quirky, but in the long run, it still helps.

🚫 Common Credit Mistakes to Avoid

I’ve seen people make the same credit mistakes over and over. Let me save you from these traps:

- Mistake #1: Closing old credit cards. Keep them open! Use them occasionally to keep them active.

- Mistake #2: Only making minimum payments. Pay your balances in full when possible.

- Mistake #3: Applying for too many cards at once. Each hard inquiry dings your score.

- Mistake #4: Ignoring your credit reports. Check them at least annually for errors.

- Mistake #5: Mixing business and personal credit inappropriately.

Let’s talk about that last one because it’s huge, especially for entrepreneurs.

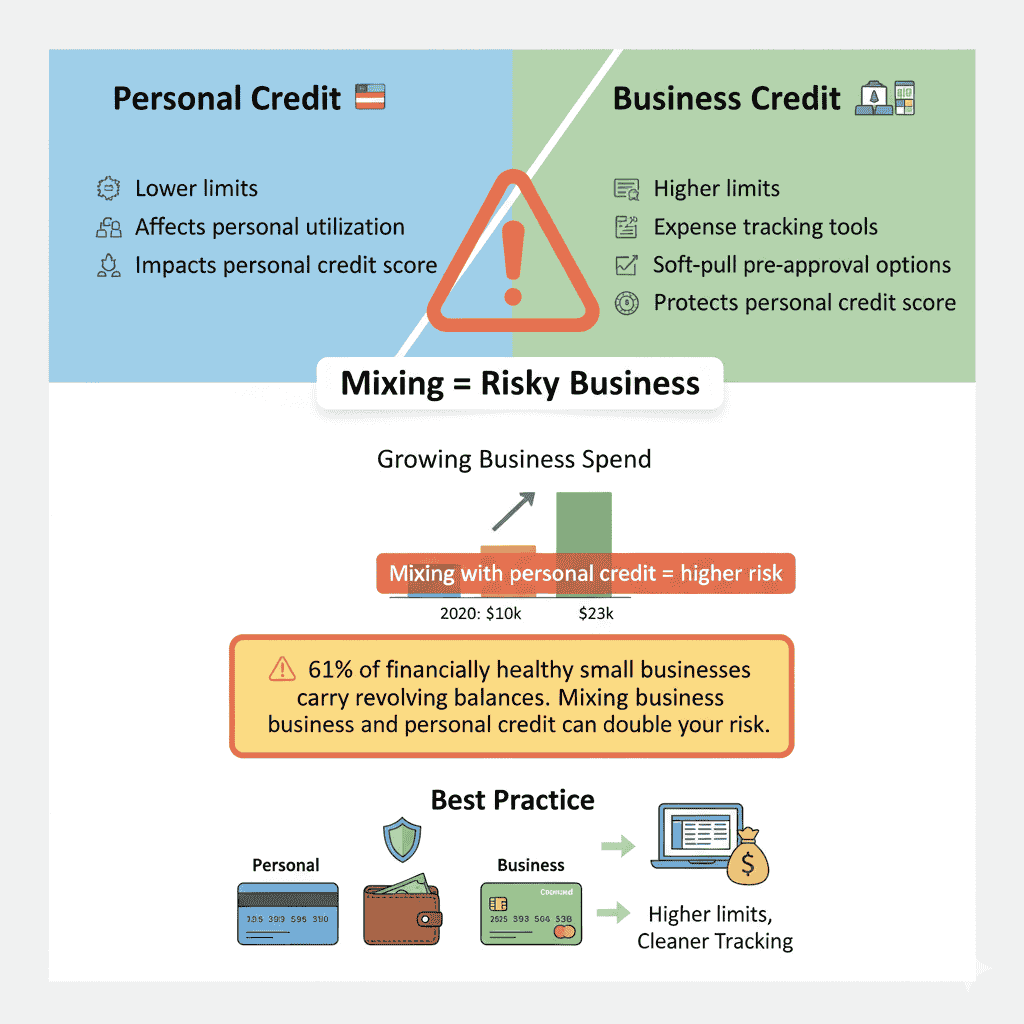

Business vs Personal Credit: Don’t Mix Them Up!

Ever wondered if you can just swipe your personal credit card for business expenses? Technically, yes. But should you? Honestly, usually not.

Here’s why:

Business credit card interest rates have jumped sharply over the past decade, the Consumer Finance Protection Bureau reports card APRs are at all-time highs, and a New York Fed analysis shows margins have kept climbing. (The exact % varies by source, but the trend is crystal clear: costs are way up.)

Meanwhile, small business owners are spending big. According to Ramp, average monthly business credit card spend nearly doubled, from around $10,000 in 2020 to $23,000 in 2025. That’s a huge amount of cash flow you don’t want tangled up with your personal utilization ratios.

And here’s the scary part: a J.D. Power study found that 61% of financially unhealthy small businesses carry revolving balances on their cards. In plain English? If your business struggles, carrying debt on a business card can already be stressful, mix that with your personal credit, and you’re setting yourself up for a double hit.

So what’s the smarter play? Get a dedicated business credit card. Not only do they usually come with higher limits and better expense-tracking tools, but many issuers also offer soft-pull pre-approval options that won’t ding your personal credit score.

At the end of the day, keeping business and personal credit separate isn’t just about staying organized, it’s about protecting your financial future.

Helpful Tools & Resources

Let me share my favorite go-to tools for credit monitoring and building. I’ve split them into free options, paid tools, and rent reporting services so you can easily decide what fits your needs.

🆓 Free Credit Monitoring Tools

- Credit Karma – Great for monitoring your score and getting alerts.

- Experian Boost – Free utility and telecom payment reporting.

- AnnualCreditReport.com – Official free reports from all three bureaus (once per year).

If you’re just starting out, these three should be your baseline.

💳 Paid Monitoring & Protection

- Experian CreditWorks – Best overall monitoring (starts $24.99/month).

- Aura – Best low-cost option.

- PrivacyGuard – Strong identity protection features.

- Credit Sesame – Offers up to $1M identity theft insurance.

Identity theft complaints in 2024 increased by 9.5% compared to 2023, and total losses related to financial scams rose by 23%, reaching $12.7 billion.

🏠 Rent Reporting Services

- Experian Boost – Free, quick impact.

- RentReporter – Paid, more comprehensive.

- Landlord programs – Ask if your landlord already participates.

💡 Consistency is key: monthly reporting is what improves your score.

💳 Credit Services Comparison Guide

| Service | Best For | Cost | Extra Benefits |

|---|---|---|---|

| Credit Karma | Free credit monitoring | Free | Score alerts |

| Experian Boost | Adding utility/rent data | Free | Immediate updates |

| AnnualCreditReport.com | Official reports | Free | One per bureau/year |

| Experian CreditWorks | Premium monitoring | From $24.99/mo | Detailed tracking |

| Aura | Budget-friendly protection | Paid | Identity monitoring |

| PrivacyGuard | Identity protection | Paid | Strong fraud alerts |

| Credit Sesame | Insurance-backed security | Paid | $1M ID theft insurance |

| RentReporter | Rent reporting | Paid | Builds payment history |

| Landlord Programs | Rent reporting | Varies | Sometimes free |

⭐ My Recommendation

- Start free with Credit Karma + AnnualCreditReport.com.

- Upgrade to Aura if you want affordable protection.

- Renters? Add Experian Boost or RentReporter so rent works for you.

The Credit-Building Mindset: Think Long, Act Small

Here’s what I want you to remember: building credit is a marathon, not a sprint. The biggest mental shift? Realizing that credit building is really habit building.

- Paying bills on time = consistent, credit-worthy behavior.

- Keeping balances low = proof you can manage credit responsibly.

Start small and keep it simple:

- Open a secured credit card.

- Sign up for Experian Boost.

- Automate your bill payments.

But here’s the thing, credit health isn’t just about scores. Another smart move is to build an emergency fund fast. Having a safety net means you won’t need to swipe credit cards every time life throws a surprise, and that stability supports your long-term credit growth.

Why rent reporting matters: On average, renters see a +23 point increase in their credit score (Experian data). That small boost could be the difference between approval or denial for your next apartment, car loan, or even a new credit card.

Conclusion

Building credit isn’t about overnight success, it’s about consistent habits over time. Every small action, paying bills on time, keeping balances low, and using reporting tools like Experian Boost or RentReporter, compounds into better financial opportunities.

Remember: Your credit score is a tool, not your worth. Focus on the long-term trend, not every tiny dip or spike.

Start small, stay consistent, and track your progress monthly. Soon enough, you’ll see the impact: easier apartment approvals, better loan rates, and more financial freedom.

Share this guide with a friend who’s starting their credit journey. Teaching others also reinforces your own habits.