I Found a Mistake on My Credit Report. Now What?

So you finally checked your credit report (good move, by the way) and boom, there’s something off.

Maybe it’s an account you never opened. Or a late payment you know you made on time. Or worse, someone else’s debt showing up under your name.

Your heart sinks. Your credit score drops overnight, and it’s not even your fault.

I get it. I’ve been there. And here’s the thing nobody tells you upfront: you’re not alone, and you actually have more power to fix credit report errors than you think.

Let me walk you through how to dispute credit report errors, step by step. No corporate jargon, no confusing legal talk. Just real strategies that actually work.

Keep reading to uncover the shocking truth about credit report errors and discover how fixing them could save you thousands of dollars, and boost your financial health!

The Shocking Truth About Credit Report Errors

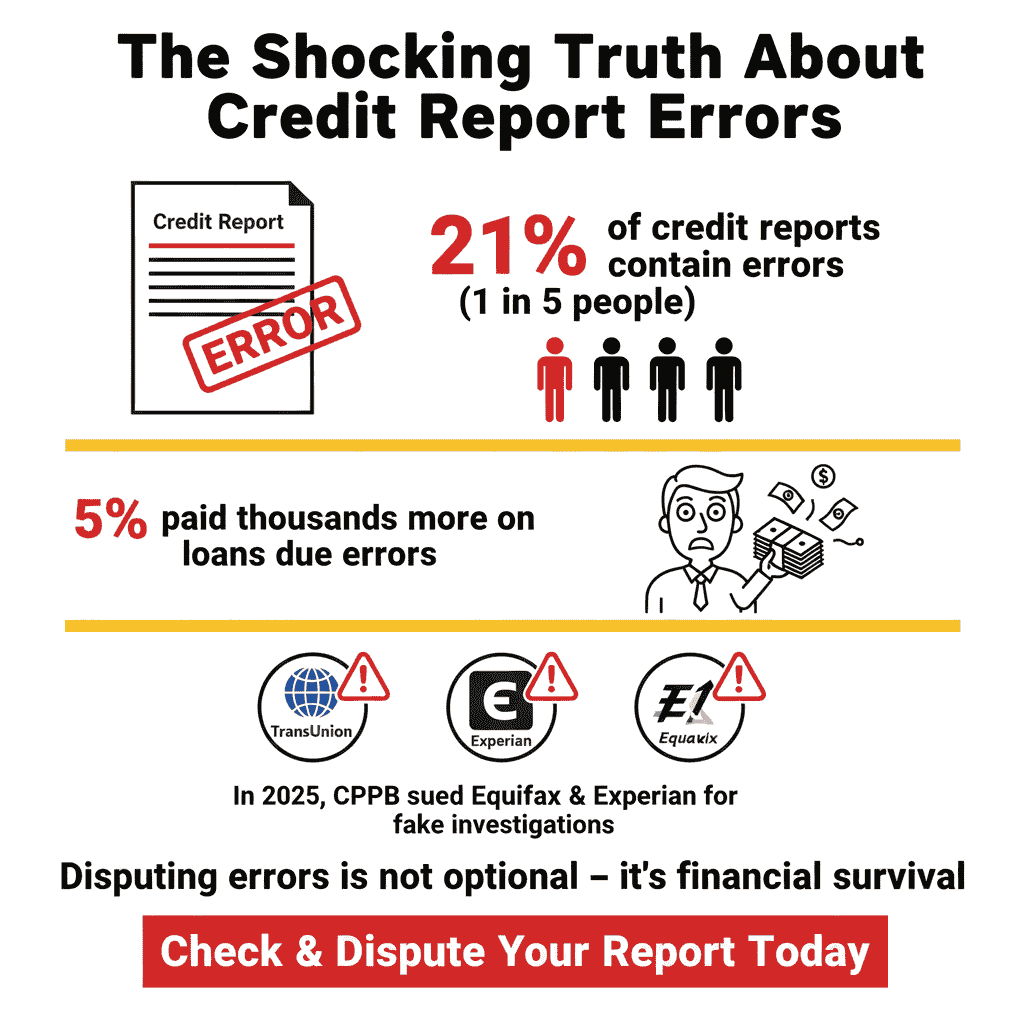

Here’s a reality check: about 21% of credit reports contain errors. That’s one in five people. Not a tiny glitch, a full-blown systemic problem.

And it gets worse: 5% of people paid more for loans because of those errors. Imagine shelling out thousands of extra dollars on a mortgage, car loan, or credit card, just because someone mishandled your data.

The part that really stings? The big three credit bureaus, TransUnion, Equifax, and Experian, are supposed to be the “gatekeepers” of accuracy. But in January 2025, the CFPB sued Equifax for relying on automated dispute investigations with little human review.

They also sued Experian for conducting “sham investigations” of credit report errors.

Yeah, you read that right. The very companies controlling your financial reputation were accused of running fake investigations.

So, when people ask: “Can I really dispute credit report errors?”, the answer is a loud YES. In fact, you should. Knowing how to dispute credit report errors isn’t optional anymore; it’s a financial survival skill.

Can You Actually Dispute Credit Report Errors? (Spoiler: Yes!)

Good news: not only can you dispute a credit report error, but the law is firmly on your side. Under the Fair Credit Reporting Act (FCRA), credit bureaus are legally required to investigate disputes, for free. They don’t have a choice.

Here’s exactly what you can dispute:

1. Personal Information Errors

- Wrong name, address, or Social Security number

- Mixed files (someone else’s info showing up on your report

2. Account Errors

- Accounts that aren’t yours

- Duplicate accounts

- Wrong account status (e.g., closed accounts showing as open)

- Incorrect credit limits or loan amounts

3. Payment History Errors

- Late payments you actually made on time

- Wrong payment dates

- Accounts showing delinquent when they’re current

4. Identity Theft Items

- Fraudulent accounts opened in your name

- Unauthorized credit inquiries

- Any debt resulting from identity theft

5. . Outdated Information

- Negative items older than 7 years (10 years for bankruptcies)

- Accounts that should have been removed from your report

Here’s the important part: you cannot dispute accurate negative information just because you don’t like it. Missed a payment? Disputing it won’t magically erase it. The dispute process exists to correct genuine errors, not rewrite your financial history.

Think of it this way: disputing credit report errors is your legal right to fix mistakes, not a magic eraser for bad decisions. When I first realized this, I couldn’t believe how much control I actually had over my own credit report.

TransUnion Dispute vs. Equifax vs. Experian: Where Do You Start?

When you’re figuring out how to dispute credit report errors, the tricky part is this: you’ve actually got three different credit bureaus, TransUnion, Equifax, and Experian.

And here’s the kicker: they don’t always have the same info on you.That means fixing an error with one doesn’t automatically fix it with the others. So let’s break it down:

📋 Credit Bureau Dispute Methods

| Credit Bureau | Online Dispute | Mail Dispute | Phone Option | Best For |

|---|---|---|---|---|

| TransUnion | Yes – Fast | Yes – Paper trail | (855) 681-3196 | Quick resolutions |

| Equifax | Yes – User-friendly | Yes – Recommended | (866) 349-5191 | Complex disputes |

| Experian | Yes – Fastest method | Yes – Traditional | (888) 397-3742 | Simple errors |

My honest take? Start with all three. I know it feels like extra work, but I’ve seen people fix something on TransUnion, celebrate, and then get shocked when the exact same error was still tanking their Equifax score. Don’t let that happen.

⚡ Pro tip: Experian says the fastest way to dispute is online. But if they reject it (and it happens), go old school, send a letter by certified mail. That paper trail is gold if you need to prove your case later.

💡 Start Your Dispute Today

✔️ Tip: File disputes with all three to make sure no error slips through the cracks.

Step-by-Step: How to Dispute Credit Report Errors (The Right Way)

Alright, let’s get tactical. Here’s exactly how to dispute credit report errors without messing it up.

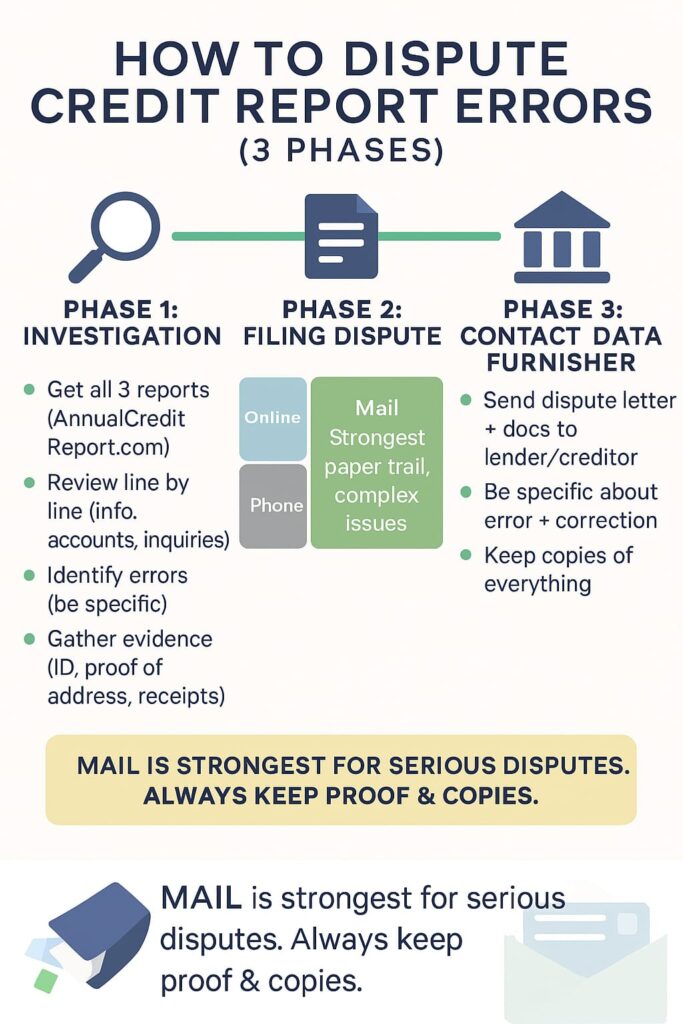

🔎 Phase 1: Investigation (Before You File a Dispute)

Step 1: Get All Three Credit Reports

Head to AnnualCreditReport.com, it’s the only official free source. You get one free report per bureau each year, but here’s a pro tip: stagger them (one every 4 months) to keep an eye on your credit year-round.

Step 2: Review Everything Carefully

Don’t skim. Go line by line and check for:

- Personal information accuracy

- Every account (open and closed)

- Payment histories

- Credit inquiries

- Public records

Step 3: Identify the Errors

Be specific. “This account isn’t mine” is stronger than “something looks wrong.”

Step 4: Gather Your Evidence

Most people skip this part, don’t. The more proof you have, the stronger your credit bureau dispute process becomes

✔️ Document Checklist:

- ✔️Copy of your credit report with errors highlighted

- ✔️Government-issued ID

- ✔️Proof of address (utility bill, bank statement)

- ✔️Supporting docs (payment receipts, bank statements, police reports for ID theft)

- ✔️Timeline of events (if relevant)

📝 Phase 2: Filing Your Dispute

You’ve got three methods to dispute credit report errors. Here’s the real breakdown:

⚖ Dispute Method Comparison

| Method | Speed | Paper Trail | Best For | Skip If… |

|---|---|---|---|---|

| Online | Fastest (instant) | Digital only | Simple, clear errors | Dispute is complex |

| Slower (7-10 days to arrive) | Strong paper trail | Complex disputes, legal issues | You need quick resolution | |

| Phone | Medium (immediate start) | Weakest (verbal only) | Quick questions | You need documentation proof |

My recommendation? Use mail for anything serious. Yeah, it’s slower, but that certified mail receipt is gold if things get messy.

How to Dispute Credit Report Online (Fastest Route):

- Go to the bureau’s dispute portal:

- Create an account or log in

- Select the item to dispute

- Choose your reason

- Upload supporting documents

- Submit & save the confirmation number

How to Dispute Credit Report by Mail (Strongest Route):

Send certified mail with return receipt to:

- TransUnion: P.O. Box 2000, Chester, PA 19016

- Equifax: P.O. Box 740256, Atlanta, GA 30374

- Experian: P.O. Box 4500, Allen, TX 75013

⚡ Phase 3: Don’t Forget the Data Furnisher

Here’s where most people slip up, disputing with the credit bureau isn’t enough.

You also need to file a dispute letter for credit report errors with the data furnisher (the bank, lender, or company that reported the wrong info).

📌 Quick tips for your data furnisher letter:

- Include the same documents you sent the bureau

- Be clear about what’s wrong and what you want fixed

- Keep copies of everything

According to the Fair Credit Reporting Act (FCRA), furnishers are legally required to investigate disputes, no matter how you file them. They can’t ignore you just because you didn’t use their “special form.”

Start Your Dispute Now

- Dispute Credit Report Online: TransUnion | Equifax | Experian

- Download Sample: Credit Report Dispute Letter Template (CFPB)

- Learn More: FCRA Dispute Rights (FTC)

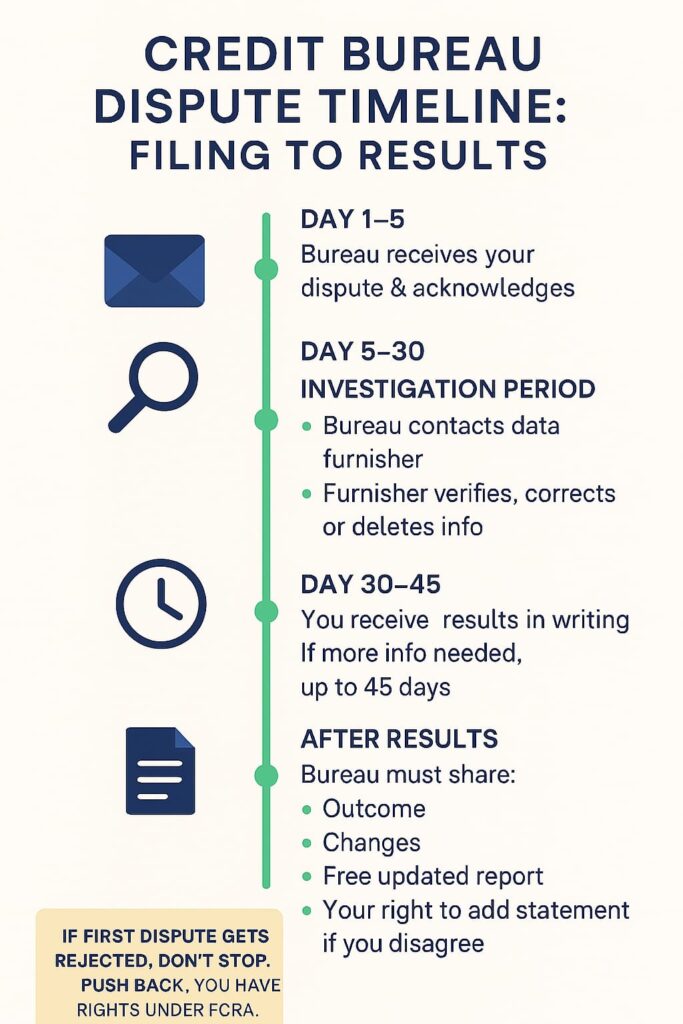

Credit Bureau Dispute Timeline: From Filing to Final Results

So you filed your dispute. Now what?

Here’s the timeline:

Days 1-5: Bureau receives your dispute and acknowledges receipt

Days 5-30: Investigation period

- Bureau contacts the data furnisher

- Furnisher reviews their records

- They verify, correct, or delete the information

Day 30-45: You get results

- If they need more info, they have up to 45 days

- Bureau must provide investigation results in writing

But let me be real with you, based on those CFPB lawsuits, not all investigations are created equal.

Some bureaus were literally rubber-stamping disputes without proper investigation. That’s why if your first dispute gets rejected, don’t give up. Sometimes you need to push harder.

The bureau must tell you:

- The result of the investigation

- Any changes made to your report

- That you can request a free copy of your updated report

- That you can add a statement if you disagree with the outcome

Fix Credit Report Errors Fast: Your 30-Day Action Plan

Want a realistic timeline? Here’s an ideal plan to fix credit report errors fast, though keep in mind, some cases stretch out.

📅 Week 1: Preparation

Day 1–2: Request all three credit reports from AnnualCreditReport.com

Day 3–4: Carefully identify errors and gather evidence

Day 5–7: Draft dispute letters / prepare online submissions

📤 Week 2: Filing

Day 8–10: File disputes with all three bureaus (online or mail)

Day 11–12: File disputes with data furnishers (banks, lenders)

Day 13–14: If using mail method, send via certified mail with return receipt

🔍 Week 3–4: Investigation

Day 15–25: Credit bureaus and furnishers investigate

Day 20–28: Monitor status updates from bureaus

Day 28–30: In many cases, you’ll receive results

Reminder: Under FCRA, bureaus generally have 30 days to complete investigation. But if you submit additional evidence during the process, the timeline can stretch to 45 days.

✔️ Week 5+: Follow Up

Review results in detail

If the error persists, escalate (file complaint with CFPB)

If corrections are made, request your updated credit report

Monitor your credit score over the next few weeks/months

✨ Pro Notes

- Always keep copies of all dispute letters, supporting docs, and certified mail receipts, they’re your proof.

- If your dispute is rejected, you can resubmit with stronger evidence or ask for a statement of dispute to be added to your report.

- Stay calm and persistent, credit bureaus face thousands of disputes daily; having documentation and following up increases your odds.

When Your Credit Score Dispute Gets Rejected (Plan B Strategies)

So you filed your dispute, waited the legally required time, and… your error is still there. Your credit score isn’t budging. Frustrating, I know.

Don’t panic. This happens more often than it should. Here are solid Plan B strategies to keep fighting:

1. Add a Statement to Your Credit File

If your dispute is denied, you can ask to insert a 100-word (or less) consumer statement in your file explaining your side. It doesn’t force a correction, but when lenders review your file, they’ll see your version of events.

Example statement:

I dispute the late payment for March 2024. I have bank records showing the payment was made March 1, 2024, before the due date.

2. Re-Dispute with Stronger Evidence

Sometimes your first try lacked compelling proof. Collect more documentation and file again. Stronger evidence might include:

- Detailed bank statements (with timestamps)

- Certified letters from creditors

- Police reports (if identity theft involved)

- Court documents or legal judgments (if applicable)

3. File a Complaint with the CFPB

This is your escalation tool.

- Go to consumerfinance.gov/complaint and submit your detailed complaint.

- Or call (855) 411-CFPB (2372). For more details USAGov

- Clearly explain what happened, provide your documentation, and state what resolution you want.

Note: Once CFPB forwards your complaint to the credit bureau or furnisher, those companies generally have 15 days to respond.

4. Dispute Directly with the Furnisher (Again)

Even if the credit bureau denies your dispute, the furnisher (bank, credit card issuer, lender) may correct the data directly.

- Send them a dispute letter with all your evidence.

- Be clear about what’s wrong and what you want fixed.

- Follow up persistently, sometimes furnishers respond where bureaus don’t.

5. Consult a Consumer Attorney

If the error is severely damaging (e.g. identity theft, large amount error) and all else fails, a lawyer specializing in consumer credit law may help. Many offer free initial consultations and sometimes work on contingency (they get paid only if you win).

⚠️ But be cautious: legal routes cost time and possibly fees. Use them when the damage or stakes justify it.

Real People, Real Results: Credit Report Dispute Success Stories

Seeing results from real folks can give you hope, and help you set realistic expectations. Below are reported credit repair success stories. These aren’t guarantees, but they show what’s possible when you do things right.

🕵️ Case Study 1: Identity Theft Recovery

- Error: 3 fraudulent credit cards opened in victim’s name

- Starting score: 580

- Actions taken: Filed a police report, disputed with all three credit bureaus, filed a CFPB complaint

- Timeline: ~45 days

- Result: All fraudulent accounts removed; credit score jumped to 698

📑 Case Study 2: Payment History Mix-Up

- Error: 6 “late payments” that were actually paid on time

- Starting score: 640

- Actions taken: Supplied detailed bank statements, disputed online (Experian)

- Timeline: ~28 days

- Result: Payments corrected; score improved to 691

🔄 Case Study 3: Multiple Errors Across Bureaus

- Error: Several inaccuracies spread across all three credit bureaus

- Starting score: 592

- Actions taken: Systematic disputes, full documentation, follow-ups

- Timeline: ~40 days

- Result: ~119-point jump to 700

⚠️ Important Note: These success stories are reported by individuals. They may not reflect every case. Some errors are more complex and take longer to correct. Use these stories to get inspired, not as guaranteed outcomes.

The Biggest Mistakes That Kill Your Credit Bureau Dispute

Before we wrap up, let me save you from the most common mistakes people make:

- ❌ Disputing accurate information (waste of time, might backfire)

- ❌ Only fixing it with one bureau (always check all three)

- ❌ Skipping the data furnisher (the source must correct it too)

- ❌ Sending weak disputes without documents

- ❌ Not following up after 30 days

👉 Want the full breakdown with 8 real examples? I’ve written a dedicated post here:

8 Common Mistakes That Can Ruin Your Credit Dispute (And How to Avoid Them)

Tools & Resources to Fix Credit Report Errors

Want to fix credit report errors the right way? Here are the legit resources to use (all free or official):

🛠 Free Credit Reports

- AnnualCreditReport.com, the only official free source (get all three reports here).

- Each bureau’s website for extra reports or account access.

📱 Dispute Portals

- TransUnion: transunion.com/credit-disputes

- Equifax: equifax.com/personal/credit-report-services

- Experian: experian.com/disputesDispute Portals

🏛 Government Help

- CFPB Complaint Portal

- CFPB Hotline: (855) 411-CFPB

- FTC Identity Theft: identitytheft.gov

- Consumer.ftc.gov, templates & guides.

⚠️ Skip “credit repair” companies. Everything they charge for, you can do yourself for free.

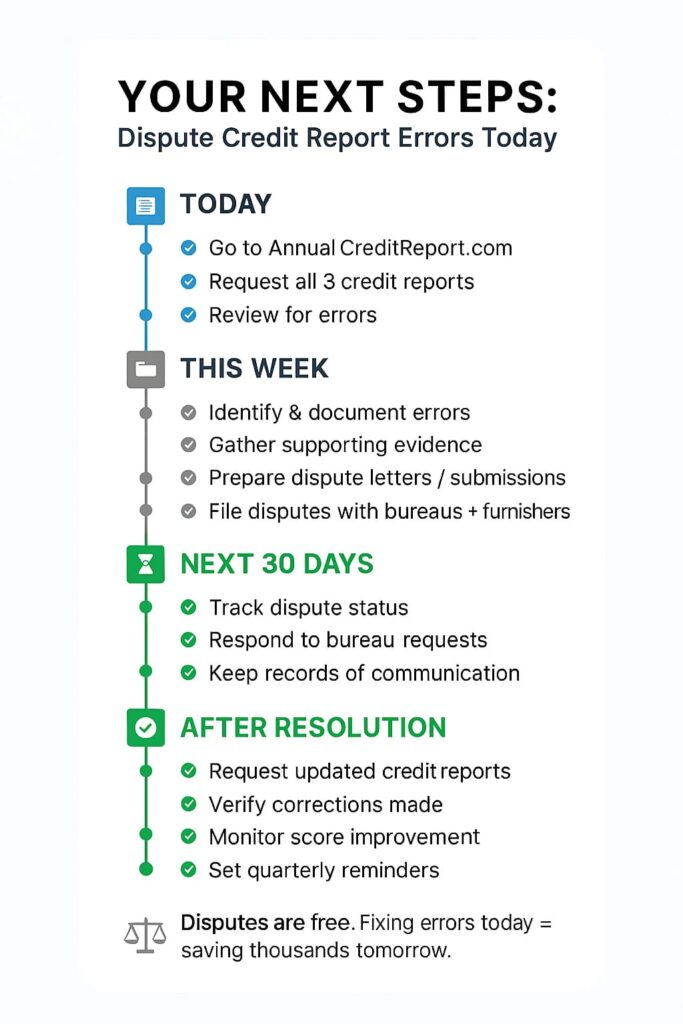

Your Next Steps: How to Dispute Credit Report Errors Starting Today

Alright, we’ve covered a lot. Let me give you a simple action plan you can start right now:

Today:

- Go to AnnualCreditReport.com

- Request all three credit reports

- Review them carefully for errors

This Week:

- Identify and document all errors

- Gather supporting evidence

- Prepare dispute letters or online submissions

- File disputes with all three bureaus (if errors appear on multiple reports)

- File disputes with data furnishers

Next 30 Days:

- Track your dispute status

- Respond to any requests for additional information

- Document all communication

- Follow up if you don’t hear back

After Resolution:

- Request updated credit reports

- Verify corrections were made

- Monitor your credit score improvement

- Set calendar reminders to check reports quarterly

Remember: You have the legal right to dispute errors for free. Don’t ignore them, every wrong entry could cost you higher interest rates and lost approvals. Fixing mistakes today can save you thousands over the life of a loan.

Final Thoughts

I know this process can feel overwhelming. The credit reporting system is complicated, sometimes unfair, and CFPB lawsuits prove the bureaus don’t always investigate properly.

But here’s the truth: 438,000 people filed complaints in 2023. That’s 438,000 people who refused to accept errors on their credit reports. Many of them got results, and you can too.

Whether you’re disputing with TransUnion, Equifax, or Experian, the steps are the same: be thorough, stay persistent, and keep documentation.

Real people see real results. One person gained 119 points in just 40 days. Your outcome may be different, but even small improvements can save you thousands over time.

So start today:

- Check your reports

- Spot the errors

- Take action to fix credit report mistakes holding you back

Your financial future is too important to let someone else’s error define it.

Want to go further? Read our Beginner’s Guide to Credit Scores for proven strategies to build and maintain excellent credit.

“Fix credit report errors today, build financial freedom tomorrow.”