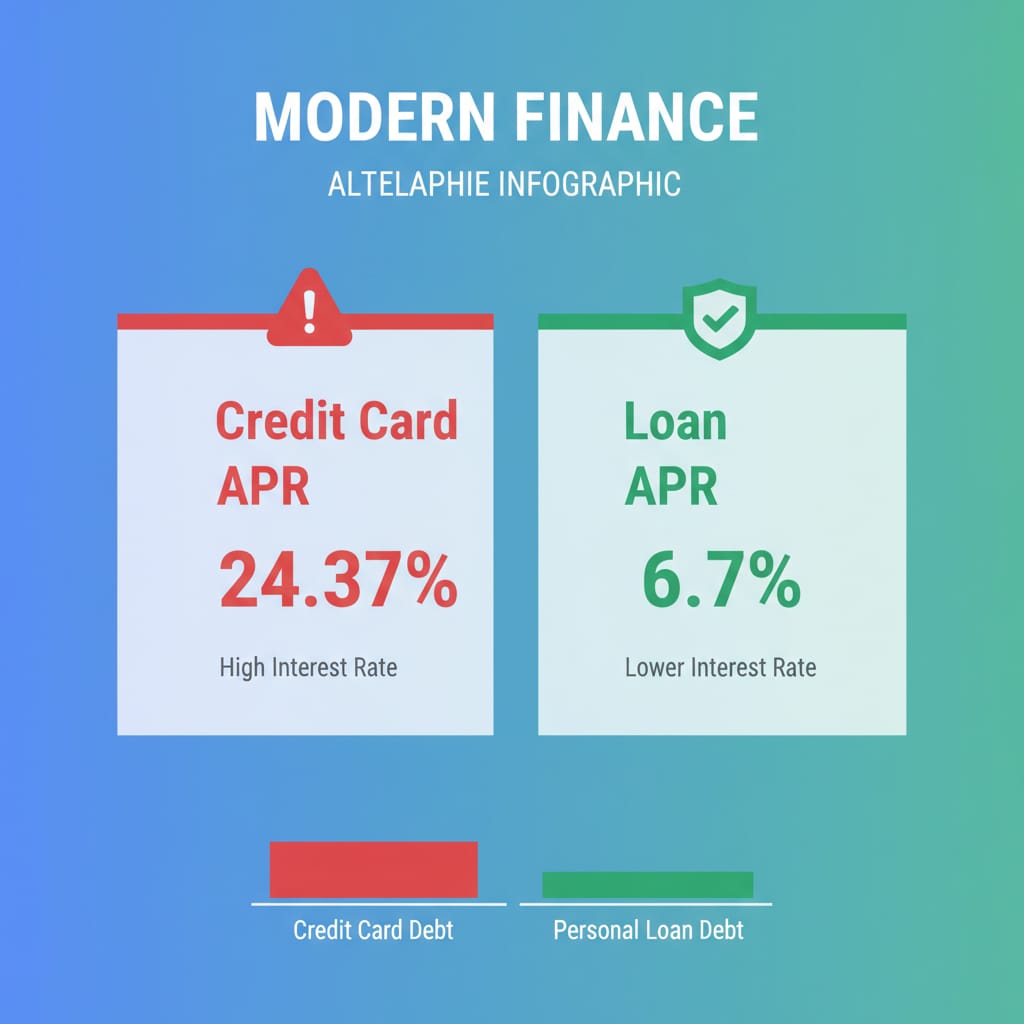

If you’re reading this in September 2025, chances are you’re feeling the financial squeeze. Nationwide credit scores just dropped by 2 points (FICO), and the average credit card APR climbed to 24.37% (Federal Reserve). That’s basically loan-shark territory, except it’s legal.

Here’s the silver lining: the best debt consolidation loans 2025 are starting at just 6.7% APR. That’s nearly one-third of today’s average credit card rate.

So why am I telling you this? Because I think you deserve better than drowning in 24% interest when there’s a life raft sitting right there.

Why 2025 is Actually Perfect Timing

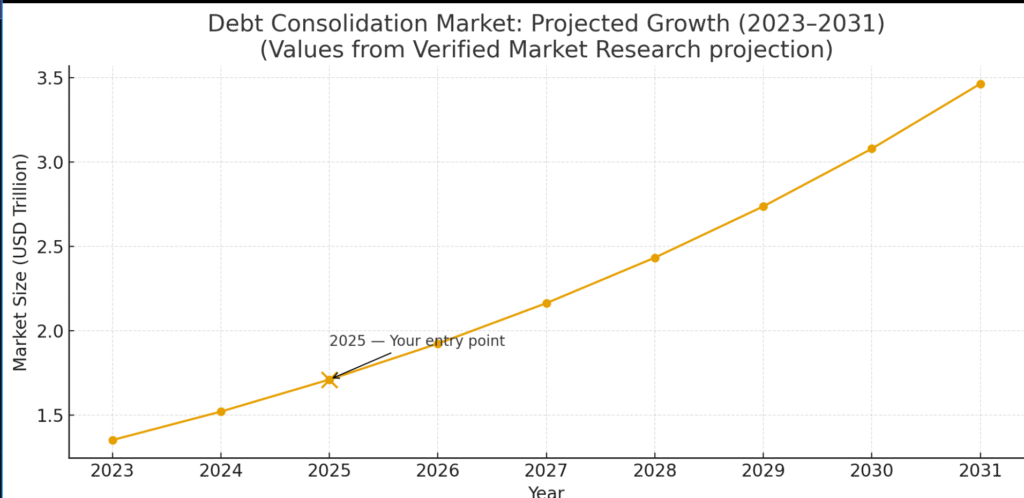

You’d think with all this chaos, loans would be harder to get. But the debt consolidation market is booming, projected to reach $3.1 trillion by 2031 (Allied Market Research).

What does this mean for you? Competition. And competition means better rates, better terms, and lenders practically fighting for your business.

I was talking to my neighbor fahreen last week (she works in banking), and she said something that stuck with me: “Right now, if you have decent credit, lenders are rolling out the red carpet.”

The irony? While everyone’s panicking about credit scores dropping, people with scores above 650 are getting some of the best deals we’ve seen in years.

Best Debt Consolidation Loans 2025

Let’s be brief. I’ve been doing the homework for weeks, so I will do you the favor.

SoFi Personal Loans, The Game Changer

Look, I’ll be honest – I used to think online lenders were sketchy. Boy, was I wrong about SoFi.

These guys offer some of the best debt consolidation loans 2025, and here’s why they’re different: zero fees. None. Not even origination fees that other lenders sneak in.

Their rates start around 8.99% for good credit, but here’s the kicker, they actually care about your financial health. These people not only provide career coaching but also help with financial planning. And if you lose your job, they also help you find a new one. It seems as if they truly want you to succeed. Weird concept, right?

Application process? Takes about 15 minutes online. Funding in 2-7 days. I’ve seen people get approved with credit scores as low as 680.

Marcus by Goldman Sachs – Still Worth a Look

Okay, so here’s the deal. Marcus, yep, the Goldman Sachs people, used to be famous for personal loans. But they actually shut that part down back in 2023 (Bankrate). If you’re reading this hoping for a shiny new Marcus loan, nope… not happening anymore.

But don’t click away just yet Marcus is still a solid option if you’re looking to grow your savings. Their High-Yield Online Savings Account is sitting at around 3.65% APY right now. That’s way better than the “thanks for nothing” 0.01% a lot of big-name banks give you.

And if you like locking in your money, Marcus also offers Certificates of Deposit (CDs) with rates hovering around 4.10%–4.25% depending on the term. Not bad if you’ve got some cash you won’t need for a while.

The best part? No minimum deposit to open their savings account, no sneaky fees, and the interface is actually clean and simple. It’s very un–Wall Street of them, and I mean that in the best way possible.

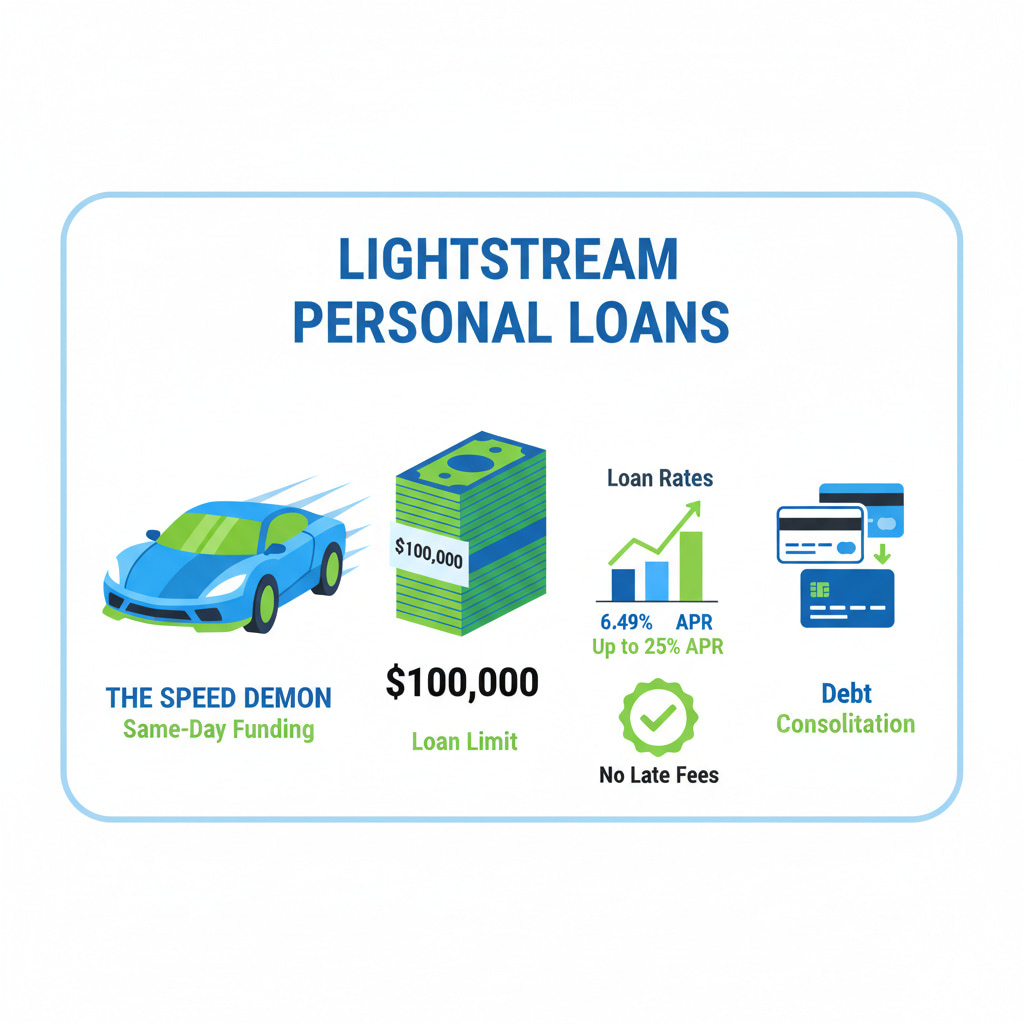

LightStream, The Speed Demon

So if you’re dead set on getting a personal loan right now, Marcus isn’t your guy anymore.

But that’s where LightStream (a division of Truist Bank) comes racing in.

If you need money yesterday, LightStream might be your best bet for debt consolidation or big-ticket loans. In fact, you can sometimes get same-day funding if you apply early enough (Bankrate).

Rates currently start around 6.49% APR with AutoPay and can go up to about 25%, depending on your credit and loan purpose (LightStream official rates). And get this, they’ll lend up to $100,000, which is more than enough to wipe out most credit card balances in one shot.

And here’s what’s wild, they don’t even charge late fees. Their philosophy is basically “life happens, we get it.” Honestly, that’s pretty refreshing in today’s world.

Bank of America, The Traditional Route

Sometimes you just want a lender you already trust. Bank of America might be that safe pick. They offer personal loans with rates ranging from about 7.5% up to ~25.5% APR, depending on how good your credit is, how much you’re borrowing, and how long you need to pay it back. (LendEDU)

If you’re already a customer with a checking account, there might be small perks or discounts, though I dug around and couldn’t find a totally reliable source that confirms the often-cited “0.25% checking account discount” for personal loans. So take that part as possible, not guaranteed.

What you get with BoA is predictability. The downside? The application can feel old-school, more paperwork, slower approvals, more checks. If you don’t mind that, and want the stability of a bank you know, this is solid. If speed is everything, though, there are more nimble lenders out there.

Wells Fargo, The Relationship Lender

Here’s one that really leans into being loyal-bank-customer-friendly: Wells Fargo gives a rate edge if you’re already banking with them.

Rates can start as low as ≈ 6.74-6.99% APR if you have a qualifying Wells Fargo checking account and enroll in automatic payments, that’s their “relationship discount.”

Loan amounts range from $3,000 up to $100,000 with fixed rates, no origination fee, and no prepayment penalty.

To qualify you’ll need to have had a Wells Fargo account open for at least 12 months and set up automatic payments from a Wells Fargo deposit account.

A few months ago, when I went to the bank, I overheard a friend say that Wells Fargo sometimes takes a slightly lenient approach to its long-term customers. For example, applicants with scores around 655 are considered because of their strong banking history. But I would say that a solid credit profile is still necessary to get the best rates.

If you don’t mind a bit of old-school paperwork and slower processing, Wells Fargo is a solid choice, especially if you value sticking with the bank you already trust.

| Lender | Focus | APR / APY | Loan Amount | Requirements | Benefits |

|---|---|---|---|---|---|

| Marcus (Goldman Sachs) |

Savings & CDs (No New Loans) |

Savings: 3.65% CD: 4.10% – 4.25% |

N/A | No min. deposit | Backed by Goldman Sachs |

| LightStream (Truist) |

Debt Consolidation Loans | 6.49% – 25% | Up to $100,000 | Excellent credit for best APR | Same-day funding, no late fees |

| Discover | Unsecured Loans | 7.99% – 24.99% | $2,500 – $40,000 | 660+ credit score | No origination fee |

| Upstart | AI-Powered Loans | 6.70% – 35.99% | $1,000 – $50,000 | Considers education, job | AI approvals |

| Wells Fargo | Loans for Existing Customers | 6.74% – 23.74% | $3,000 – $100,000 | Customer (12+ months) | 0.25% discount |

How to Actually Qualify (The Real Talk)

Here’s where I’m gonna get real with you. All these great rates I mentioned? They’re for people with excellent credit. If your score took a hit recently (and let’s face it, many did), you’re looking at higher rates.But don’t give up yet.

Credit Score Reality Check

Most lenders want to see at least 650 for approval. For the best rates on debt consolidation loans, you’re looking at 720+.

But here’s something interesting – the recent 2-point drop everyone experienced? Lenders are actually being pretty understanding about it. They know it’s not really your fault.I talked to a loan officer at SoFi, and she said they’re looking at the bigger picture now. Consistent payment history over the last year matters more than a small score dip.

| Credit Score Range | Category | Approval Chance | Interest Rate Expectation |

|---|---|---|---|

| <580 | Poor | Very Low | Very High APR |

| 580–669 | Fair | Possible but Tough | Higher than Average |

| 670–739 | Good | Solid Chance | Better Rates Available |

| 740–799 | Very Good | High Chance | Low Rates, Strong Terms |

| 800+ | Excellent | Best Chance | Lowest Rates Available |

Income Requirements

Lenders often look for stable income for at least two years. But “stable” doesn’t necessarily mean you have to stay in the same job, your income flow should be consistent. Gig economy workers, freelancers, even people with variable commission, they’re all getting approved.

The key is showing consistent earning ability. Bank statements, tax returns, and if you’re self-employed, profit-loss statements are usually requested. This means the documentation needs to be quite detailed.

The Math: How Much You Save

My neighbor joshua? He had $45,000 in credit card debt spread across five cards. Average interest rate? 23.8%.

New payment? $850 a month. Payoff time? 5 years and 3 months.

His minimum payments were $1,200 per month, but the principal was making almost no difference. Imagine, at this pace, it would have taken him 47 years to clear everything. Yes, a full 47 years!

Then he was approved for a solid debt consolidation loan, $45,000 at a 9.5% rate.Total interest saved? Over $89,000.

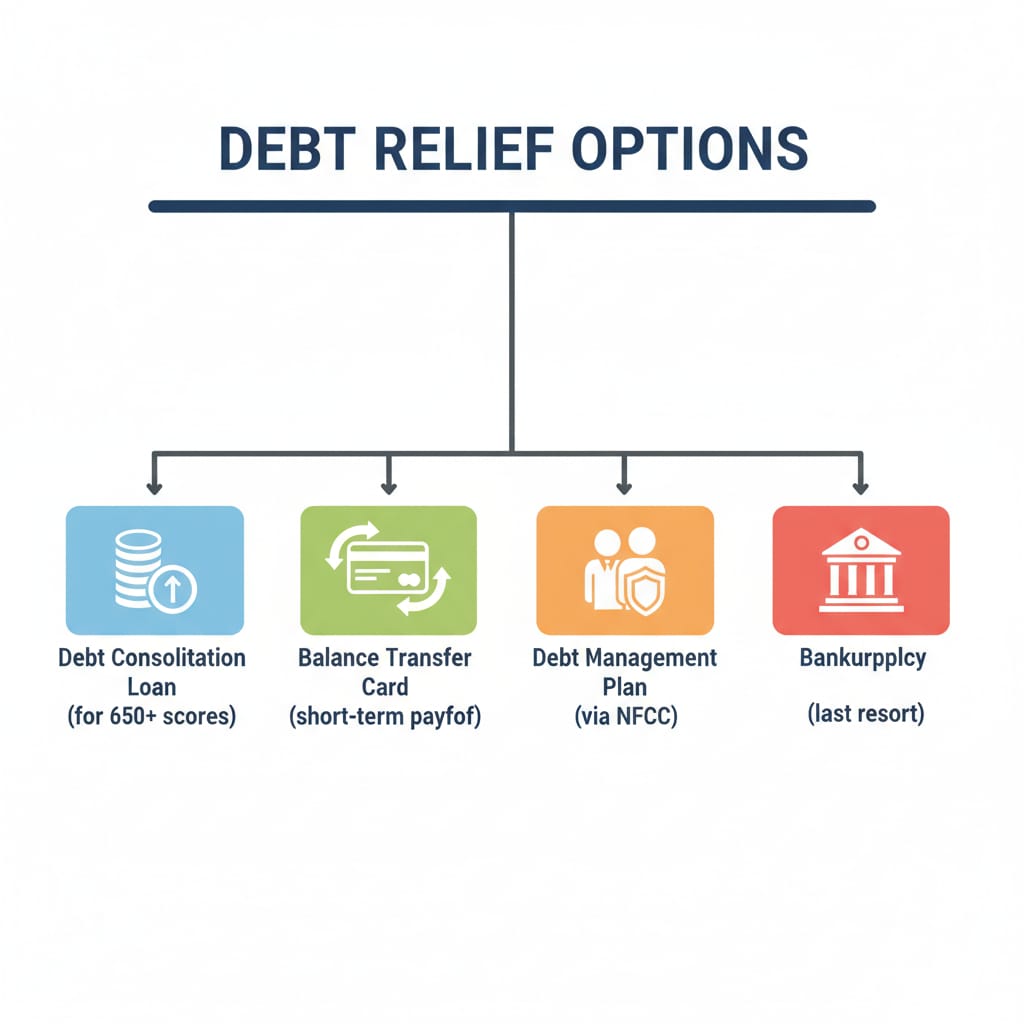

When Debt Consolidation Isn’t Right (Yes, I’m Being Honest)

Look, I believe in the best debt consolidation loans 2025, but they’re not magic. There are times when other options make more sense.

If You’re Barely Making Minimums

If you can’t comfortably make the new consolidation loan payment, you’re just setting yourself up for failure.

In this case, a debt management plan can be a very good option. You may be able to negotiate lower rates with your creditors through a credit counseling agency. Yes, the process is a little longer, but payments are often lower than those of a consolidation loan.

If You’re Considering Bankruptcy

If your debt-to-income ratio is above 40%, consolidation will only delay the inevitable. Sometimes bankruptcy provides the fresh start that is truly necessary. I know it sounds scary, but Chapter 7 bankruptcy can discharge credit card debt entirely.

Talk to a bankruptcy attorney before committing to any debt consolidation loans 2025.

If You Haven’t Fixed Your Spending

This is the big one. If you consolidate your credit cards but don’t change your spending habits, you’ll just run up the cards again. Now you’ve got the old debt PLUS new credit card debt. This looks like a complete nightmare.

But it’s important to be honest with yourself, have you ever thought about why you got into debt in the first place?

Job loss, medical bills, overspending? If it’s overspending and you haven’t addressed it, consolidation won’t help.

Balance Transfers vs Consolidation Loans

Sometimes a 0% APR balance transfer card (e.g., Citi Simplicity) is better, if you can pay off in 18–21 months.

Risk: fail to pay before promo ends = rates higher than consolidation loans.

Success Stories

- Marcus (not the bank): $38k → LightStream loan at 11.2% → $724/month → Debt-free in 5.5 years. Credit score rose +67 points in 6 months.

- Maria: $29k, score 578 → DMP → paid off in 4 years. Score now 701, recently bought her first home.

- My brother do this successfully with $18,000 in debt. He got a Citi Simplicity card with 21 months at 0%, made payments of $857 per month, and was debt-free in 21 months. Total interest paid? Zero.

But in my opinion, he’s the most disciplined guy. He put the card straight back in the drawer and treated it as if it didn’t exist, until all his debt was cleared.

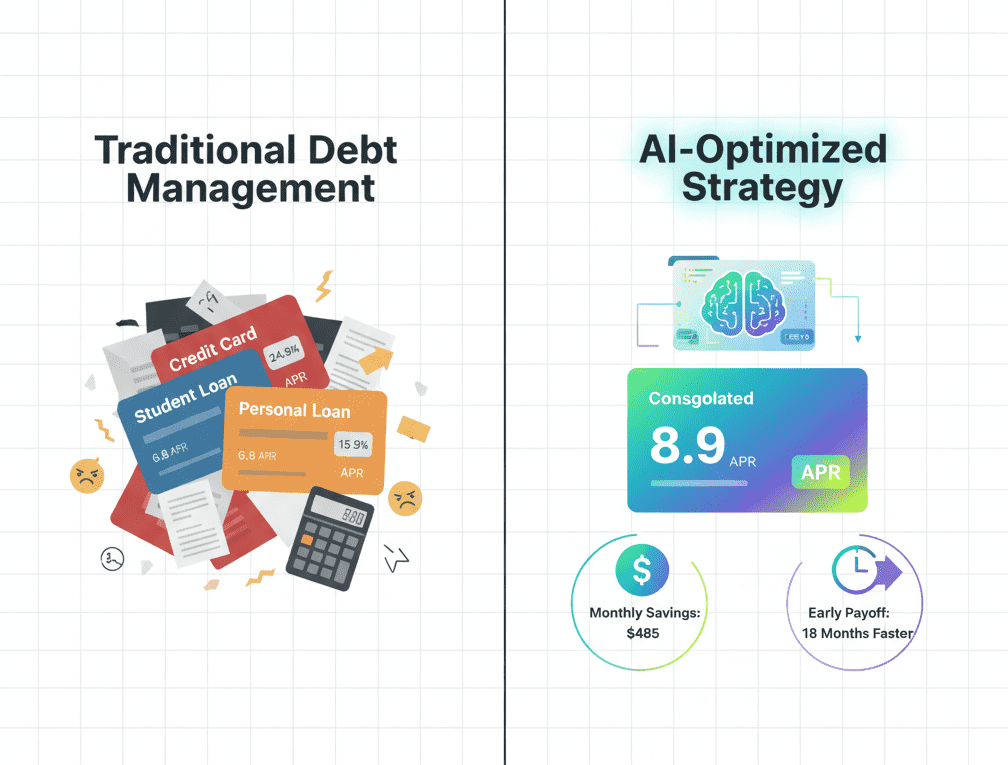

The AI Revolution in Debt Management

You know what? There’s something pretty exciting happening in personal finance right now, and most people don’t even realize it. AI is quietly taking over debt management, and honestly, it’s about time.

Think about it: instead of you manually juggling credit cards, student loans, and personal debts (we’ve all been there), AI can now do the heavy lifting. These smart systems track your spending, spot where you’re overspending, and actually suggest better ways to tackle your debt. Pretty cool, right?

But here’s the really interesting part, we’re not talking about basic calculators anymore. These are dynamic solutions that learn from your behavior and adjust in real time. It’s like having a personal financial advisor that never sleeps.

Companies like SoFi Relay are already doing this – giving you the complete picture of your finances in one place. And behind the scenes, fintech companies like Method are making it possible for apps to integrate these AI features seamlessly.

The bottom line? If you’re struggling with multiple debts (and let’s be honest, who isn’t these days), this AI revolution is genuinely good news. The technology is getting scary good at personalizing solutions that actually work.

What Financial Advisors Don’t Want You to Know

This happened a few months ago. I went out for coffee with a friend of mine. We were just talking, and he said something that completely took me by surprise. He’s a financial advisor, by the way.

He said, most of my clients could handle their debt consolidation themselves, but they pay me $200 an hour to basically fill out applications for them.”

The truth? Getting the best debt consolidation loans isn’t rocket science. It’s paperwork and patience.

Dave’s process:

- First, check your credit scores from all three bureaus.

- Then, calculate your total debt and what you want your monthly payment to be.

- Within 14 days, apply to 3–5 lenders (multiple inquiries within this window count as one on your credit report).

- Compare the offers and pick the best option.

That’s it. No magic, no special connections, just a bit of legwork.

Your Action Plan

Alright, here’s where the rubber meets the road. You’ve read all this, you’re probably feeling a mix of hope and overwhelm. That’s normal.

1. Market Analysis

Check current rates: Credit cards at 24.37% vs consolidation loans starting at 6.7%. Understand the massive savings opportunity.

2. Credit Assessment

Get your credit score from all 3 bureaus. Need 650+ to qualify, 720+ for best rates. Recent 2-point drops are being overlooked by lenders.

3. Research Options

Compare consolidation loans vs balance transfers vs debt management plans. Consider SoFi (no fees), LightStream (speed), and traditional banks.

4. Apply Smart

Apply to 3-5 lenders within 14 days (counts as one credit inquiry). Have documents ready: tax returns, pay stubs, debt list.

5. Execute & Save

Choose best offer, pay off credit cards, and enjoy single monthly payment. Potential savings: $89,000+ over loan term with disciplined approach.

Final Thoughts: Your Debt Consolidation Journey Starts Now

The best debt consolidation loans 2025 aren’t just numbers on a screen, they’re your ticket out of the 24% interest rate trap that’s keeping millions of Americans stuck.

The Bottom Line

2025 presents a rare opportunity. While credit scores are dropping nationwide, lenders are competing harder than ever for qualified borrowers. Translation? If you have a 650+ credit score and stable income, you’re in the driver’s seat.

Take Action Today

Remember Joshua’s $89,000 savings? That wasn’t luck, it was smart decision-making. The longer you wait, the more interest compounds against you.

Don’t Wait for Perfect Timing

Perfect timing doesn’t exist in personal finance. Good timing does. And right now, with consolidation loan rates starting at 6.7% APR, the timing couldn’t be better.

FAQS

-

What is a debt consolidation loan?

Debt consolidation loan = one new loan to pay off all your smaller debts.

Pros:

1. One payment instead of many → way easier to manage.

2. Lower interest (sometimes) → can save you money if your new loan has a better rate.

3. Clear payoff plan → fixed term, so you know when you’ll be debt-free.

4. Credit score boost (maybe) → if you pay on time and lower your credit card balances.Cons:

1. Not always cheaper → if your interest rate isn’t better, you might pay more.

2. Longer repayment = more total cost → monthly payments may be smaller, but stretched over years = more interest overall.

3. Fees → some lenders charge origination fees or penalties.

4. Temptation to spend again → if you clear credit cards but keep swiping them, debt can pile up twice as fast. -

How to pay off $30,000 in debt in 1 year?

Okay, let’s talk real talk here. Paying off $30,000 in just one year is a big challenge, but it’s not impossible if your income is solid and you’re ready to hustle hard. Here’s the point-to-point breakdown:

1. Do the math → $2,500/month just for debt.

2. Cut expenses → drop non-essentials, live lean.

3. Boost income → side jobs, overtime, sell stuff.

4. Use a strategy → avalanche (highest interest first) or snowball (smallest debt first).

5. No new debt → lock away those credit cards.

6. Consider consolidation → only if it lowers interest and you stay disciplined. -

Is a debt consolidation loan a good idea?

1. You get a lower interest rate than what you’re paying now.

2. You want one simple monthly payment instead of juggling many.

3. You have a clear payoff plan and won’t add more debt on top.But it’s not a good idea if:

1. The new loan’s interest is higher or about the same as your current debt.

2. You just want temporary relief but keep swiping your credit cards.

3. Fees (like origination fees or penalties) eat up the savings. -

Is a debt consolidation loan a good idea?

There’s no fixed max for debt consolidation loans. It depends

on your credit, income, and the lender.

Many lenders cap around $50k–$100k.

Some credit unions/banks may go higher (even $150k+).

Secured loans (like home equity) usually allow larger amounts than unsecured ones.