Have you ever opened your bank account, seen that it’s nearly empty, and wondered where all your money went?

I think this happens to everyone. I still remember the end of the month when I only had $15 left and my salary was still a week away. This kind of stress can take you to a whole different world.

I realized that budgeting shouldn’t be seen as a boring spreadsheet but as a powerful money management tool that we should take advantage of. The biggest benefit is that it gives you control over your money.

In this guide, I’ll teach you how to create a personal or family budget. My goal is to explain complex things in an extremely simple and practical way. So, let’s get started.

Step 1: Calculate Your Net Income

If you want to learn how to create a personal or family budget, first you need to know your net income, because it’s crucial to understand it. This means figuring out how much money you have left after taxes to run your household. You’ll need to count everything.

Consider this your starting point, because without clarity, it’s impossible to budget.

If you have deductions like retirement contributions (401k) or insurance automatically taken out, add them back in temporarily so you know your true earnings.

Step 2: Track Your Current Spending

For one to two months, track all your expenses. You need to know what, how much, and where you’re spending. There are many tools available for this.

TOOL’S

1. Spendee

- Supports multiple wallets or currencies.

- Easy charts and graphs for spending overview.

- Manual entry plus Bank sync limited (in free plan)

- The family sharing option is also there.

2. Monefy

- It is a very simple and lightweight app.

- 1 tap expense adding system is fast entry.

- You can customize some categories.

3. Money Manager expense & budget

- Daily monthly report is given.

- Budget setting or debt management options.

- Completely free with ads (premium version also but not necessary)

4. AndroMoney

- Multi platforms (Android, iOS, Web).

- Budgeting alert and multiple accounts handling.

- Free with ads but highly reliable

Step 3: Choose a Budgeting Method

| Method | Best For | Pros | Cons |

|---|---|---|---|

| 50/30/20 Rule | Beginners | Simple, flexible | Difficult with tight budget |

| Zero-Based Budgeting | Detailed planners | Every dollar assigned | Time-consuming, strict |

| Envelope Method | Families | Helps control overspending | Hard with cards/online payments |

Step 4: Budget Category Percentages (A Guideline)

| Category | % of Income | Example ($3,000 Income) |

|---|---|---|

| Housing | 25–30% | $750–$900 |

| Food | 10–15% | $300–$450 |

| Transportation | 10–20% | $300–$600 |

| Savings & Investments | 10–15% | $300–$450 |

| Insurance & Healthcare | 5–10% | $150–$300 |

| Fun / Discretionary | 5–10% | $150–$300 |

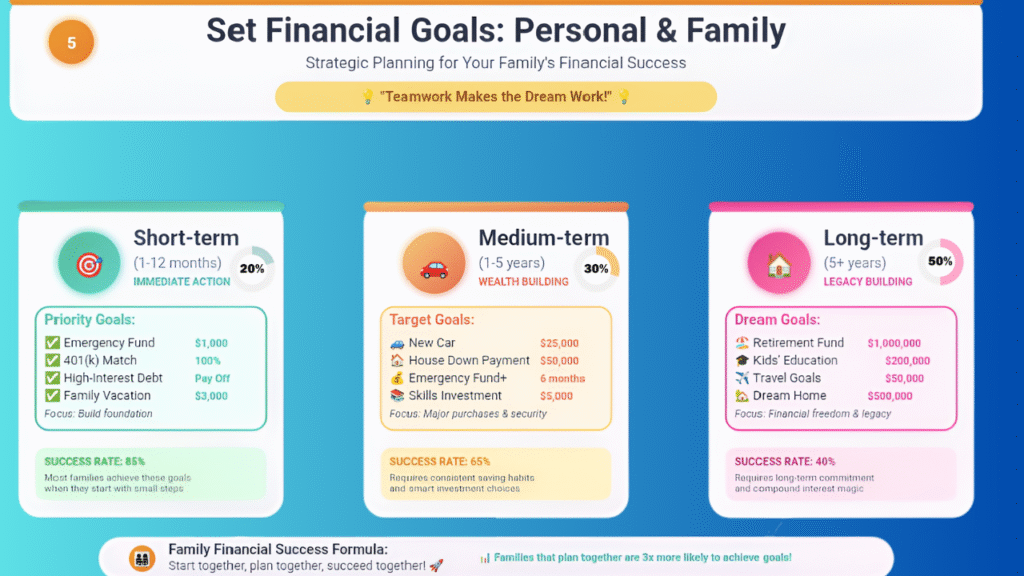

Step 5: Set Financial Goals (Personal & Family)

- Short-term (1–12 months): Emergency fund, vacation.

- Medium-term (1–5 years): Car, house down payment.

- Long-term (5+ years): Retirement, kids’ education.

- Emergency fund

- Employer 401(k) match (if available)

- Pay off high-interest debt

- Retirement savings

- Build bigger emergency fund

- Other debt

- Lifestyle goals (travel, upgrades)

When it comes to family budgeting, I think we should involve everyone, because teamwork builds motivation. And haven’t you heard the line, “Teamwork makes the dream work”?

Step 6: Use Budgeting Tools

TOOL’S

Budgeting Tools Comparison Table

| Tool | Price | Method/Style | Pros ✅ | Cons ❌ | Best For |

|---|---|---|---|---|---|

| Mint | Free | Automatic sync, categories | Easy to use, free alerts, bill tracking | Limited customization | Beginners |

| YNAB | Paid ($14.99/month, free trial) | Zero-based budgeting | Deep insights, goal tracking, habit building | Paid subscription | Serious budgeters |

| Goodbudget | Free & Paid | Envelope system (manual) | Family sync, manual control | Time-consuming manual entry | Couples & families |

| PocketGuard | Free & Paid | Simplified cash flow | Shows “In My Pocket” money, prevents overspending | Limited features in free version | Daily spend control |

| Excel / Google Sheets | Free | Customizable (manual) | 100% flexible, templates available | No automation, requires discipline | DIY budgeters |

Step 7: Review & Adjust Monthly

Whenever you review your budget, be sure to check where you spent too much and where you could have saved.

For example, you went out to eat and ended up spending more than you wanted to. That’s okay, it’s common and happens to everyone. But what does a smart person do? They adjust it next time.

Review your goals as well. Check if you achieved your savings and investing goals. For example, your goal was to save $500 a month, but you only saved $300. (Again, no big deal). Next time, reduce your unnecessary expenses to get closer to your goal. If possible, be sure to ask your loved ones for help.

A special quote for you: “Alone we can do so little; together we can do so much.” (Helen Keller)

Step 8: Build Good Money Habits

- Pay yourself first (auto-savings).

- Use the 24-hour rule for impulse buys.

- Hold a monthly family budget meeting.

- Automate bills and savings.

Common Mistakes vs. Fixes

| Mistake | Fix |

| Overly strict budget | Allow for “fun money” |

| Ignoring annual costs | Create a “sinking fund” |

| Quitting after one bad month | Treat it as a learning process |

Conclusion

Remember: Budgeting isn’t just about saving money; it’s a roadmap that gives you financial freedom along with the freedom to live your life. For example:

Peace of mind:

- An end to the stress of every bill or debt.

- Money is always ready for emergencies.

So, once you take control of your spending, you’ll realize that money is finally working for you, not against you. The best budget is the one you can stick with. Start small, stay consistent, and celebrate wins along the way.