You checked your credit report. You spotted an error. You filed a dispute.And… nothing happened.Or worse, your dispute got rejected.

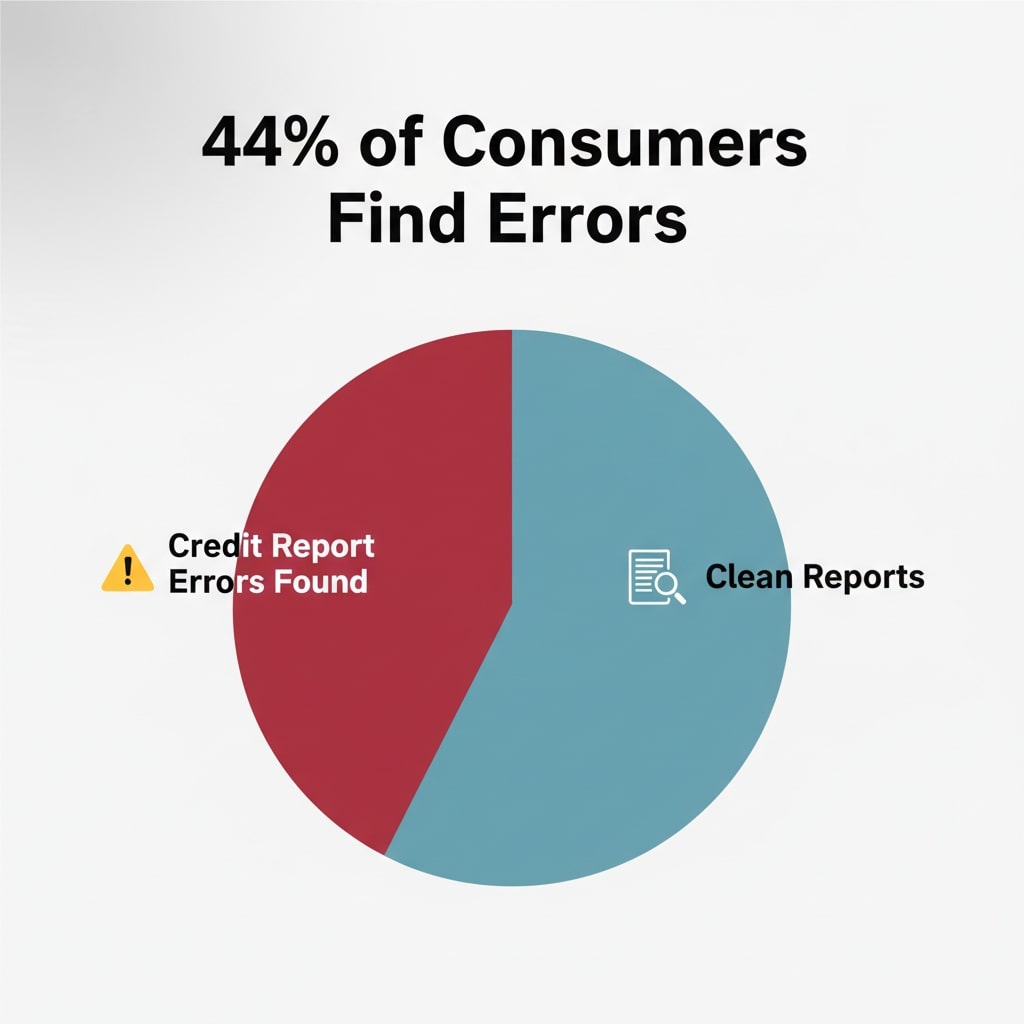

Here’s a hard truth: a 2024 study by Consumer Reports and WorkMoney found that 44% of people discovered at least one error in their credit reports. That’s nearly half of all consumers checking their files. Yet, most disputes still fail, not because the errors aren’t real, but because people make avoidable mistakes in how they try to fix them.

And it isn’t just consumer error. In January 2025, the CFPB fined Equifax $15 million for failing to properly investigate disputes. Regulators have also criticized Experian for running what the CFPB called “sham investigations.”

So yes, the system is stacked against you. But that doesn’t mean you’re powerless.

In this guide, I’ll walk you through the most common mistakes people make when trying to fix mistakes on credit report, why these errors tank disputes, and, most importantly, how to handle the process the right way so your corrections actually stick.

Why Your Credit Dispute Probably Failed (And Why That’s Not Your Fault)

You filed a dispute. But nothing changed, or it got rejected. You may have done your part right. But the system? It’s flawed.

In 2023, the CFPB reported over 1.3 million complaints, nearly 79% tied to credit and consumer reporting issues. In many cases, credit bureaus relied too heavily on creditors’ data instead of verifying evidence provided by consumers.

So yes, your dispute might have failed not because you did something wrong, but because the process is stacked.

But that doesn’t mean you resign yourself to bad credit. Understanding how to fix mistakes on credit report gives you control. Even if the system is weak, you can force results if you use the right evidence and method.

Mistake #1: Only Checking One Credit Bureau

A common but costly mistake: checking just one credit report and assuming you’re in the clear.

Here’s the problem, Equifax, Experian, and TransUnion are separate companies. They don’t share updates. An error fixed with one bureau doesn’t automatically disappear from the others.

Take this real case: a consumer spent months removing a late payment from Equifax. Success. But when her landlord pulled TransUnion, the same error still dragged down her score, and cost her the apartment.

The fix? Always review all three reports. The only official free source is AnnualCreditReport.com.

Pull reports from each bureau and compare them line by line.

If the same error appears on multiple reports, you must dispute with each bureau separately. They won’t “copy-paste” corrections.

Pro tip: stagger your free checks, TransUnion in January, Equifax in May, Experian in September, so you’re monitoring year-round.

Bottom line: If you want to truly know how to fix mistakes on credit report, you can’t stop at one bureau. All three matter.

Mistake #2: Your Dispute Letter Looks Like Everyone Else’s

Most people Google a “credit dispute letter,” copy a template, and send it off. No surprise, those disputes usually fail. Why? Because credit bureaus process millions of disputes every year, and generic language gets flagged or ignored.

It’s not paranoia either, the CFPB sued Experian for “faulty intake procedures”, meaning many disputes weren’t even properly reviewed. If your letter looks like every other template, chances are slim it’ll get taken seriously.

Bad dispute letter (everyone uses):

“This account is wrong. Please investigate and remove it. Thank you.”

Good dispute letter (that actually works):

“Account #1234-5678 from ABC Bank shows a 30-day late payment dated March 15, 2024.

This is incorrect.

I paid on March 1, 2024 (confirmation #ABC123).

Attached is my bank statement.

This error is damaging my credit score.

I request immediate correction under FCRA Section 611.”

See the difference? Specific details + evidence + legal backing. That’s how you learn how to fix mistakes on credit report with a letter that gets taken seriously.

Checklist for a solid dispute letter:

- Full name & current address

- Account number / item in question

- Dates, amounts, and error explanation

- Why it’s wrong, with documented evidence

- What you want corrected

- Copies of proof (never send originals)

- Signature

Pro tip: Dispute one error per letter. If you lump multiple issues together, half might get ignored.

Takeaway: Ditch the templates. Write each dispute like a case, specific, professional, and evidence-based.

Mistake #3: You’re Ignoring the Personal Information

Most people jump straight to balances and late payments, but skip the personal information section of their credit report. Big mistake.

Just in 2023, the FTC received 1.1 million identity theft reports, making it the number-one consumer complaint. And the numbers aren’t slowing down, FTC data shows identity theft cases continued to climb in 2024, with fraud and scam reports hitting record highs.

For example, in 2024 alone, Florida reported 115,840 identity theft cases, with losses totaling $866.1 million. Georgia had 55,955 cases and $291.3 million in losses. Both states crossed 500 cases per 100,000 residents, earning them the label of fraud “hotspots.

FTC 2024 data shows the top 10 states for identity theft, with Florida and Georgia leading the pack. Source: Federal Trade Commission.

”Bottom line? The personal info section of your credit report isn’t filler. It’s where the earliest warning signs of identity theft often appear.

How to Fix Personal Info Mistakes on Your Credit Report

- Get your reports. Pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and look for mistakes.

- Dispute errors. File a dispute with the credit bureau online, by mail, or by phone. Be clear about what’s wrong, why it’s wrong, and include supporting documents like ID, utility bills, or letters that verify the correct info.

- Include the details. Add your contact info, credit report confirmation number, and mark or circle the disputed items on a copy of your report.

- If mailing, do it right. Send disputes by certified mail with “return receipt requested” so you have proof it was delivered.

- Investigation process. The credit bureau will check with the company that provided the info. If the error is confirmed, they’ll fix or remove it. If the info is accurate, it will stay.

- Contact the source directly. You can also reach out to the lender or company that reported the data, sometimes that speeds things up.

- Escalate if needed. If you’re unhappy with the bureau’s response, escalate within the bureau or file a complaint with an external agency.

- Add a consumer statement. If the error isn’t fixed, you have the right to add a statement to your report explaining your side.

Fixing personal information errors makes sure your credit report is accurate and up to date, a must for protecting your credit score, loan approvals, and overall financial health.

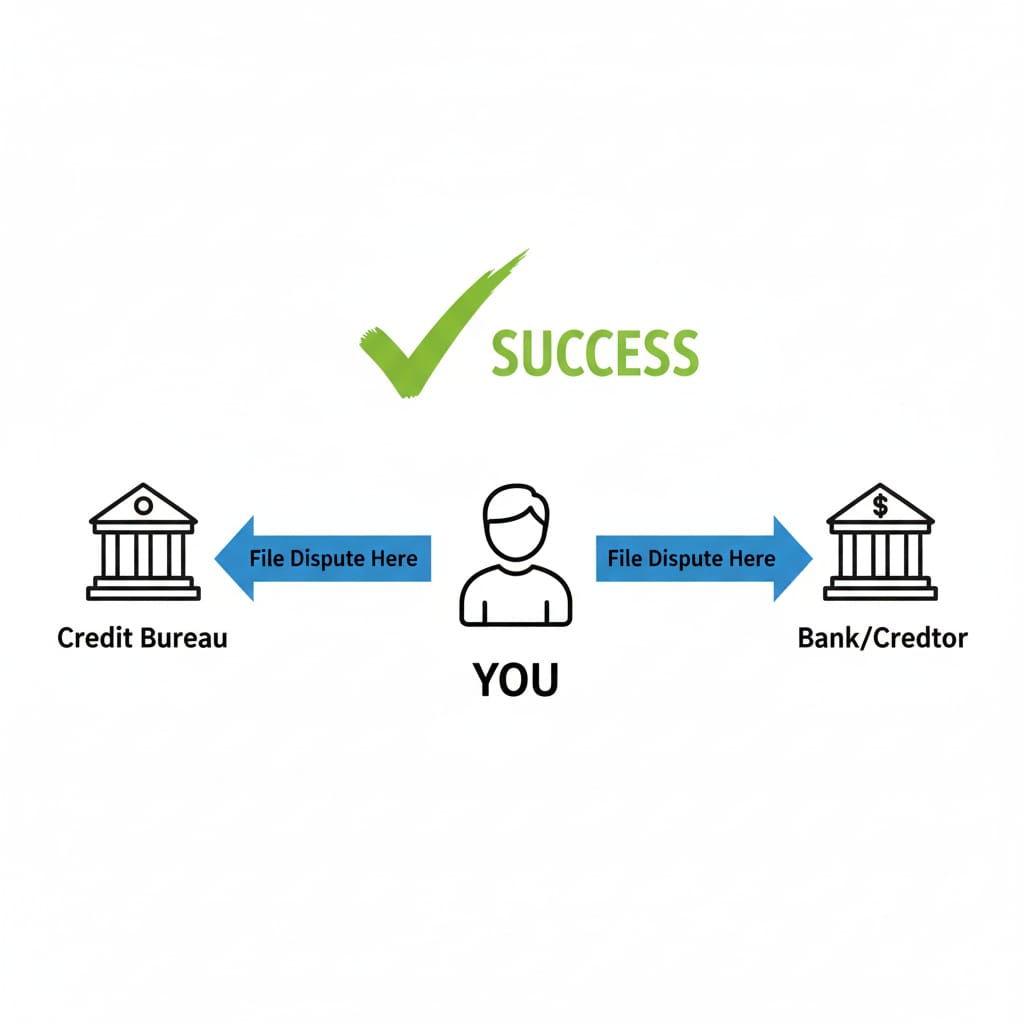

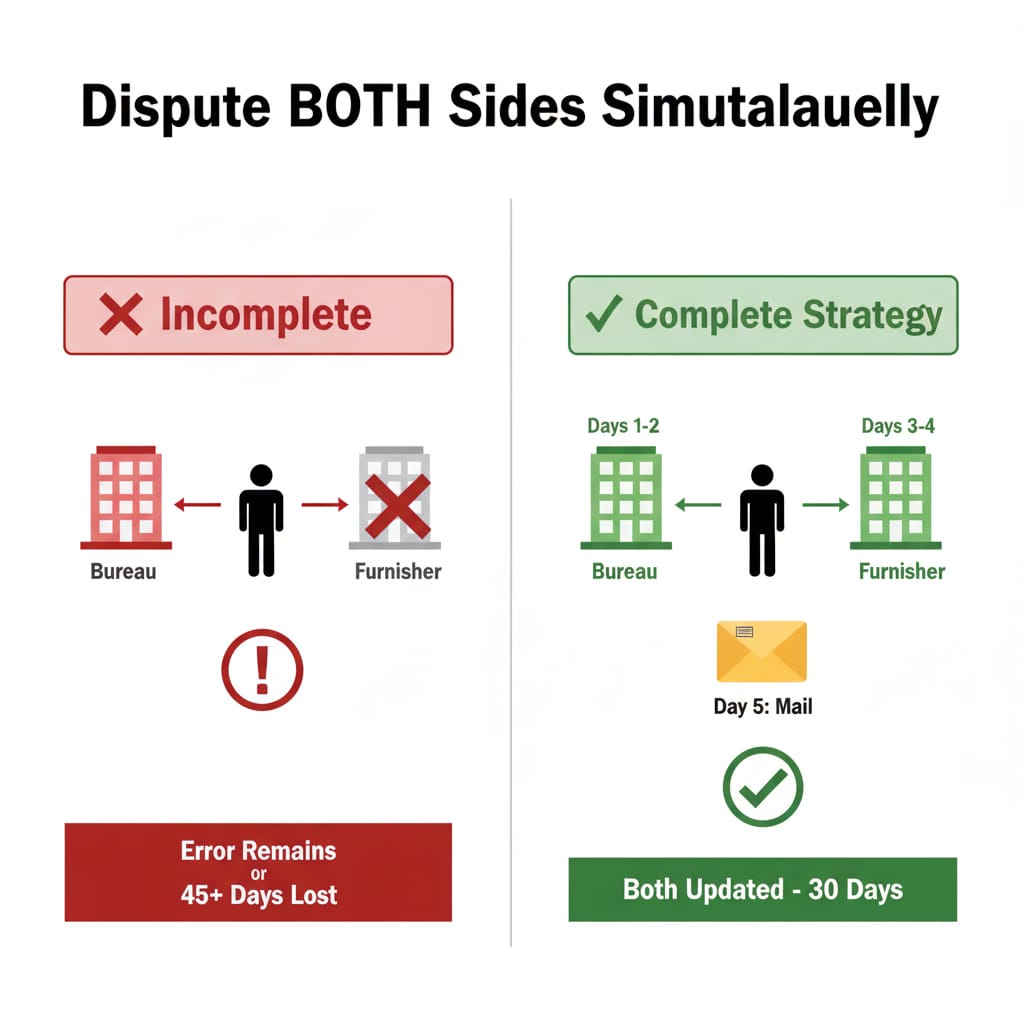

Mistake #4: You’re Fighting Half the Battle

Here’s where people get tripped up on how to fix mistakes on credit report: they only dispute with the credit bureau.

But here’s the catch, bureaus don’t verify much themselves. They simply ask the bank or creditor (the “data furnisher”) whether the info is accurate. If the furnisher says “yes,” your dispute often gets rejected. You lose 30 days and gain nothing.

File two disputes simultaneously:

- One with the credit bureau (TransUnion/Equifax/Experian)

- One with the data furnisher (the bank, credit card company, whoever)

This creates pressure from both sides.

The bureau has to investigate under FCRA Section 611. The furnisher has to investigate under FCRA Section 623. And if the furnisher admits they were wrong, the bureau has to update your report.

How to Identify Your Credit Data Furnisher

Here are the steps to figure out which company reported the information on your credit report.

Key Steps for Identification

1. Look at the Account Section of Your Credit Report:

- Next to the details for each credit account, you’ll see the name or institution that reported that account. This company is your “data furnisher.”

2. Check for Contact Information:

- The credit report often includes the furnisher’s contact details, sometimes right under the account information or in a separate section. This is the address you’ll use to send a dispute.

3. If You Can’t Find Contact Info:

- Simply Google the company’s name to find their official customer service or dispute resolution department’s address.

4. Check the Credit Bureau Websites:

- Sometimes, the credit bureaus themselves (Experian, Equifax, TransUnion) list furnishers or their contact information on their websites.

Mistake #5: Don’t Try to Erase Accurate Information

Let’s be honest, some “credit repair” companies claim you can dispute anything and it might get removed on a technicality. Sometimes it happens, but mostly, it doesn’t work, and it can backfire.

Under FCRA Section 611(a), if you repeatedly dispute information that’s actually accurate, credit bureaus can label your disputes as frivolous. This means they can legally stop investigating your disputes altogether, even the legitimate ones.

So, if you honestly missed a payment, disputing it won’t make it vanish. The credit bureau investigates, the lender confirms the missed payment, and your dispute is rejected. Persisting only risks your future disputes being ignored.

What You Can’t Dispute (Because It’s True)

- Late payments you genuinely made

- Debts legitimately in collections

- Accurate bankruptcies or foreclosures

- Hard inquiries you authorized

What You CAN Dispute (Even If the Account Exists)

- Incorrect dates on accounts

- Wrong balances or amounts

- Accounts past the 7-year reporting limit (10 years for bankruptcy)

- Duplicate entries for the same debt

- Incorrect account status (e.g., marked open when closed)

It’s about correcting errors, not rewriting your financial history.

Feeling Down About Accurate Negatives?

It’s tough to see negative marks on your report, but disputing them won’t help. Instead, focus on building positive credit habits:

- Make on-time payments consistently

- Maintain low credit utilization

- Consider a secured credit card if your credit is damaged

Want to improve your credit beyond disputing errors? Check out our guide on how to build and repair your credit the smart way.

REMEMBER, the credit system keeps accurate negatives visible for seven years, but trying to game the system usually makes things worse. Playing the long game with good habits is your best bet.

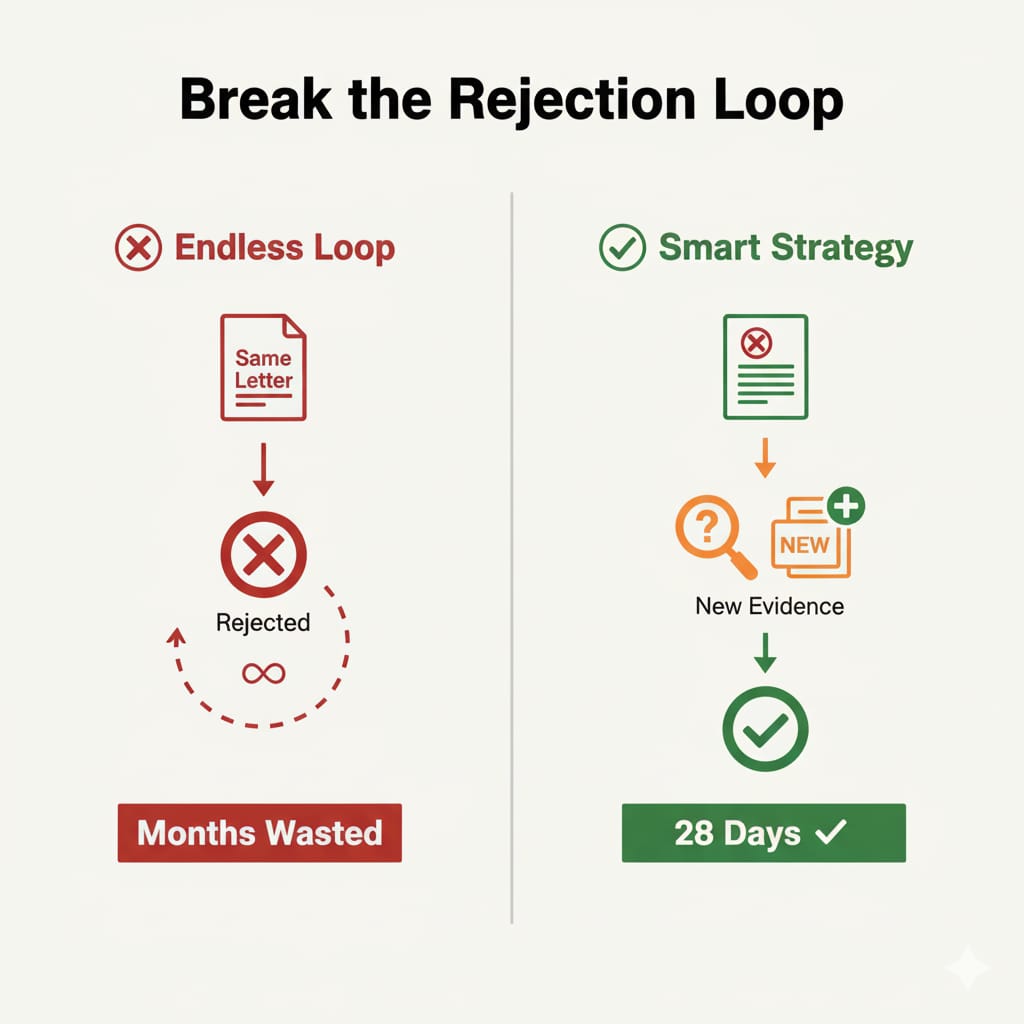

Mistake #6: You Keep Sending the Same Thing Over and Over

It’s frustrating, but understandable.

Your dispute gets rejected. You’re upset. So you send the exact same dispute letter again, maybe with slight wording changes. It gets rejected again. So, you try a third time.

The credit bureau’s response? “We’ve already investigated this, stop sending it.”

Here’s the key about fixing mistakes on your credit report when your first dispute fails: You need NEW evidence. Not just the same proof with a new cover letter. Actual new information they haven’t seen before.

Under the FCRA regulations, bureaus can reject “repeated” disputes that lack substantial new information. They have a legal right to ignore disputes that simply repeat previous claims.

What Counts as New Evidence?

- Additional documents you didn’t send before

- Updated account statements

- A letter from the creditor admitting an error

- Court documents

- Police reports for identity theft cases

What Does NOT Count as New Evidence?

- The same bank statement with different highlights

- Emotional pleas (“please, this is really important”)

- Threats without legal backing

- Rewording the same claim over and over

The Right Way to Handle a Rejected Dispute

- Carefully read the rejection reason. Why was it denied?

- Find evidence that directly addresses that reason.

- Wait a few days, don’t resend immediately out of frustration.

- Send a new dispute with the fresh evidence, and reference your previous dispute’s confirmation number.

- If rejected again despite strong new evidence, escalate to a CFPB complaint instead of resending identical letters.

I knew someone who sent the same dispute seven times in eight months, each time no new evidence. Naturally, it failed every time. When they finally added a creditor’s letter admitting the error, it was resolved within 28 days.

Persistence is good. Repeating the same failed approach? That’s just wasting precious time.

Mistake #7: You Called the Bank But Forgot the Credit Bureau (Or Vice Versa)

A common error is disputing only with the bank or only with the credit bureau.

Sometimes, companies fix records internally but don’t update credit bureaus, so errors stay on your report. Other times, bureaus confirm info with companies who approve without checking, leading to failed disputes.

How to Fix:

Dispute both the credit bureaus (Experian, Equifax, TransUnion) and the data furnisher simultaneously.

Timeline:

- Days 1-2: Dispute with bureaus

- Days 3-4: Dispute with furnisher

- Day 5: Send via certified mail (if applicable)

- Day 30: Check responses

If one fixes the issue but the other doesn’t update, send proof of correction to the lagging party.

Example: James disputed a wrong $2,500 balance with Equifax, but the credit card company wrongly confirmed it accurate. After direct dispute plus payoff letter to the company, they corrected records and informed bureaus. Time lost: 45 days.

Tip: Do both disputes from the start to avoid delays.

Mistake #8: Your Filing System is “I’ll Remember This”

Picture this:

You send a dispute. You’re confident. Weeks later the bureau replies: “We never got your letter.”

And now you’re stuck, because… you didn’t keep proof.

Sound familiar? That’s the danger of relying on memory.

🪞The Reality Check

Your brain is not a filing cabinet.

You will forget confirmation numbers.

You will mix up dates.

And you’ll definitely lose track of “who said what” on phone calls.

🛠️The Fix: Build a Paper Trail

- Keep copies of every letter and doc you send

- Save certified mail receipts (with tracking numbers)

- Screenshot online disputes

- Write down notes from every call (date, time, rep name, reference number)

🤔Why Bother?

- Certified mail = no more “we never got it” excuses

- Notes prove investigations were rushed or sloppy

- Records become your ammo if you escalate to the CFPB

🗂️ How to Stay Organized

One simple folder → physical or digital, doesn’t matter. Inside it:

- Original reports (errors highlighted)

- Every piece of correspondence

- Your notes + timeline of actions

- All responses from bureaus & furnishers

💡 Pro Move

Keep a basic spreadsheet with columns like: Date | Action Taken | Bureau/Furnisher | Confirmation Response Due

Outcome

Next Step.

It looks boring… until the day you win a dispute because you had the receipts.

Mistake #9: You Slept on the Deadline

Imagine this: You spot an error on your credit report. You mean to fix it, but life gets busy.

By the time you circle back, the bureau has already closed your dispute. Why? Because you missed their deadline.

That’s how most people lose, not on facts, but on timing.

⏳ The Rules of the Game

Under the Fair Credit Reporting Act (FCRA), credit bureaus have 30 days to investigate once they get your dispute.

➡️ If you add new info mid-investigation, that window can stretch to 45 days.

➡️ But if you drag your feet and don’t reply quickly? They can shut your dispute down, end of story.

🕒Timing Traps to Avoid

- 7-year rule: Most negatives fall off after 7 years (bankruptcies = 10). But in some states, disputing too close to the deadline might actually restart the clock.

- Old debts: Disputing past the statute of limitations can wake up sleeping collectors.

- Identity theft: Here, every minute matters. File a police report right away, freeze your credit within 24–48 hours, and hit fraudulent accounts fast.

📅 How to Stay on Top of Deadlines

- File disputes ASAP, there’s no “perfect time.”

- Set reminders:

- Day 15 → check status

- Day 28 → follow up

- Day 32 → escalate if silence continues

- Reply to bureau requests within 5 days max.

- Double-check how old a negative item is. If it’s about to fall off, sometimes waiting is smarter.

💥 Reality Check

Missing a deadline doesn’t just waste 30–45 days, it can also derail a loan approval, cost you a job offer, or jack up your interest rates.

Timing is leverage. Use it, or lose it.

Mistake #10: You Stopped After the Bureau Said No

Your dispute gets rejected. You’re frustrated. Maybe you try once more, it gets rejected again. So you give up.

I get it. The system feels rigged because, honestly, it kind of is. But here’s what most people don’t know: A rejection from the bureau isn’t the end of the road. It’s just the end of that road.

There are escalation options that actually work.

Plan B when your dispute gets rejected:

Option 1: Add a consumer statement to your file

You get to add a 100-word statement to your credit report explaining your side. It doesn’t remove the error, but when lenders review your report, they see your explanation.

Example: “I dispute the late payment for March 2024. I have documentation showing timely payment on March 1, 2024. The creditor has not adequately addressed this evidence.”

Does it fix your score? No. But it shows you’re actively addressing it and gives your side of the story.

Option 2: File a CFPB complaint

This is the nuclear option, and it works.

Go to consumerfinance.gov/complaint and submit a detailed complaint about the bureau’s inadequate investigation. The CFPB will forward it to the bureau, and suddenly your dispute gets taken seriously.

Companies have to respond within 15 days. And they know the CFPB is watching.

In 2023, consumers filed 645,000 complaints. The CFPB doesn’t ignore these. Neither do the bureaus when they’re on the receiving end.

Include everything: Timeline of your disputes, evidence you submitted, why the bureau’s investigation was inadequate, what you want fixed.

Option 3: Go back to the furnisher with escalation

If the bureau won’t listen, pressure the furnisher directly.

Call, ask for a supervisor. Reference FCRA Section 623. Mention you’re documenting this for a potential CFPB complaint.

Write to their CEO or compliance officer (not customer service). Companies have investor relations pages with executive contacts.

Sometimes the squeaky wheel approach works when the polite approach didn’t.

Option 4: Legal help (when it’s worth it)

If the error’s causing significant financial harm, denied mortgage, lost job, thousands in higher interest, consult a consumer attorney.

Many work on contingency (they only get paid if you win). FCRA violations can result in actual damages plus $100-$1,000 per violation plus attorney fees.

Find one through the National Association of Consumer Advocates (consumeradvocates.org).

I’m not saying sue over a $50 error. But a $20,000 fraudulent debt that’s been “investigated” three times and keeps getting verified? Yeah, that might be worth legal action.

My take: The bureaus count on you giving up. Don’t give them that satisfaction.

If you’ve got solid evidence and they’re still rejecting you? Fight back. Use the CFPB. Escalate. Be the person who doesn’t quit.

Because here’s the thing about how to fix mistakes on credit report: Sometimes the only way to fix it is to make more noise than they’re comfortable ignoring.

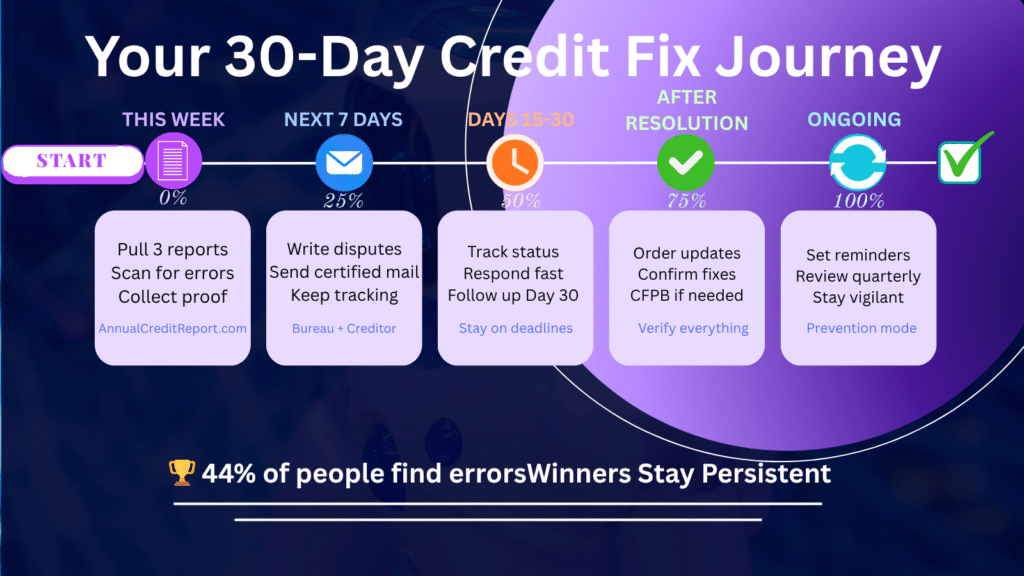

Your Quick Action Plan

- This Week: Pull all 3 credit reports from AnnualCreditReport.com. Check personal info, scan every account, and note errors with dates/amounts. Collect proof (statements, receipts, screenshots).

- Next 7 Days: Write a separate dispute letter for each error. Send to both bureaus and creditors. Use certified mail and keep tracking slips. Stay organized with a simple folder or spreadsheet.

- Days 15–30: Track your disputes online or by phone. Respond quickly if they ask for more info. If no reply by Day 30, follow up firmly.

- After Resolution: Order updated reports to confirm corrections. Still wrong? File a CFPB complaint or talk to a credit expert.

- Ongoing: Set reminders to review your reports every few months.

REMEMBER: 44% of people find errors on their credit reports. The winners? They stay persistent.

Here’s the Truth Nobody Wants to Say Out Loud

Credit bureaus make money from having your data. They don’t make money from fixing your data.

Banks and creditors report information, sometimes carelessly, because they’re juggling millions of accounts and your one error isn’t their priority.

The whole system relies on you not knowing how to fix mistakes on credit report properly, giving up after the first rejection, or being too intimidated to push back.

And for years, it worked. People just accepted whatever showed up on their reports.

But in 2025, things changed. The CFPB started actually holding these companies accountable. $15 million fine for Equifax. Lawsuit against Experian. Suddenly there’s at least a little bit of pressure on them to do their jobs.

You’re not powerless here. You just need to know the rules better than they expect you to.

Avoid these ten mistakes:

- Check all three bureaus

- Write specific, detailed disputes

- Don’t ignore personal information errors

- Dispute with bureau AND furnisher

- Only dispute actual errors

- Bring new evidence if rejected

- Always contact both sides

- Keep detailed records

- Mind the timelines

- Don’t give up after rejection

Do these things right, and you’ve got a legitimate shot at fixing those errors. Do them wrong? You’ll waste months getting nowhere and probably end up paying thousands more in interest while you’re stuck in limbo.

The choice is yours. The bureaus are counting on you to give up.

Don’t let them win.

Ready to dive deeper into the complete dispute process? Check out our step-by-step guide on how to dispute credit report errors for the full walkthrough. And if you’re looking at the bigger picture of credit improvement beyond just fixing errors, our guide on how to build and repair your credit covers strategies for when disputing isn’t enough.

Your credit report doesn’t have to be perfect. But it should at least be accurate. Go make that happen.